If someone gets a credit card and builds his credit up to above 800, then he doesn't use his credit card for a while like one month, one year, etc., will his credit score remain at his previous score or will it start to come down automatically?

-

3if your credit score is that high, stop obsessing about it– pboss3010Commented Jun 18, 2021 at 11:25

-

2Be aware that some banks will close accounts for inactivity; you should put a candy bar or something on it every 3-6 months if you want the credit line to stay on your reports.– ceejayozCommented Jun 18, 2021 at 13:48

-

Credit scores work differently in different countries. Where in the world are you?– VickyCommented Jun 18, 2021 at 18:48

-

@Vicky: United States.– user109157Commented Jun 19, 2021 at 2:00

-

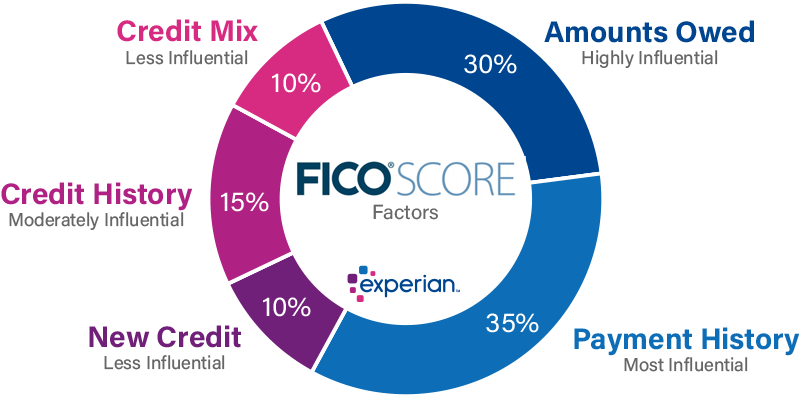

If you're saying that someone with only a single credit card could have a score north of 800 then think again. Realistically, the only way this happens is if they had other types of accounts (i.e., mortgages or car loans), because credit mix is about 10% of score. That one card would have to have a high limit and lengthy history to be such a huge score influence.– RiverNetCommented Jun 22, 2021 at 11:09

Add a comment

|

2 Answers

During the first few months of the COVID crisis, my family reduced the amount of money we were putting on our cards. For one or two seldom used cards their usage dropped to zero for several months in a row. There was no impact to the score.

Several categories related to the score would not be impacted by reducing your utilization. The age of the accounts would continue to improve; the lack of late payments would improve...

If the utilization was to drop to zero because that was the only credit card, then it is possible that your score could drop a few points. That is because utilization of your credit cards does factor into your score. Zero utilization is not need for a perfect score, in fact having a zero is a slight drag on your scores. Achieving non-zero doesn't require you to carry a balance it just requires you to charge a couple of items each month. Put a utility bill on the card, or when you get gas, and you will never have a zero utilization.

The thing you want to avoid is to have the bank cancel the card for non-use. That will impact age of accounts, amount of credit (which will increase utilization). As long as we avoid a 2008-2009 credit crisis then the simple act of one or two transactions a month will keep the card alive.

answered Jun 18, 2021 at 16:29

-

1I assume this is a US-specific answer, which may or may not be what the OP needs as credit scores work differently in different places. Can you edit to indicate what jurisdiction this applies to?– VickyCommented Jun 18, 2021 at 18:49

This is for United States only.

Low credit utilization isn't particularly harmful; actually, it's generally considered more ideal when factoring it into credit score computations.

Just use the card often enough to ensure that the issuer doesn't cancel it. That will hurt the score, because total available credit is also a large factor in the computations.

Source: experian1

Amounts Owed

"In either case, it's best to keep your utilization under 30%. Those with the best credit scores tend to use under 10% of their available credit."

Length of Credit History

"If you decide to close a credit card account in good standing, it can remain on your credit report for up to 10 years, and could continue to help your credit scores during that time. However, closing an account reduces your overall available credit, which could have a negative effect on your scores."

^ (same logic can be used if your issuer cancels the card)