I was young and stupid and opened up a Best Buy credit card 5 years ago. I bought a new laptop and also a lot more stuff during these 5 years. I have bought over 10,000 dollars worth of stuff and paid it all off today. The interest rate on the card is 24.something percent.

Due to personal financial reasons, I was not able to take advantage of low rate offers from Best Buy on stuff I bought on the card and ended up paying a whole bunch of money as interest.

I want to close this credit card for several reasons:

- It doesn't have a Mastercard/Visa/etc logo on it so I can only use it at Best Buy.

- The interest rate is ridiculously high.

- I spend more money because I get enticed into offers that come with this card. But I do not want to spend any more money than I can afford.

- I will have to pay annual maintenance fee even if I don't use this card.

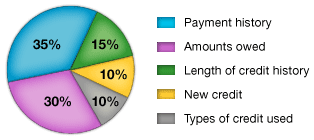

My question is, if I close this card which has a 4000 dollar credit limit on it, will it affect my credit score or credit history? Does it make sense for me to keep it open or just close it permanently? Will my total credit limit go down as a result as this card is not offered by a major credit card provider?