According to the black scholes model, volatility is one of the variables to calculate the fair price of an option. However, it doesn't specify which volatility should I use. Should I take the annualized standard deviation or should I use the implied volatility?

Add a comment

|

2 Answers

Option pricing models used by exchanges to calculate settlement prices (premiums) use a volatility measure usually describes as the current actual volatility. This is a historic volatility measure based on standard deviation across a given time period - usually 30 to 90 days.

During a trading session, an investor can use the readily available information for a given option to infer the "implied volatility". Presumably you know the option pricing model (Black-Scholes). It is easy to calculate the other variables used in the pricing model - the time value, the strike price, the spot price, the "risk free" interest rate, and anything else I may have forgotten right now. Plug all of these into the model and solve for volatility. This give the "implied volatility", so named because it has been inferred from the current price (bid or offer).

Of course, there is no guarantee that the calculated (implied) volatility will match the volatility used by the exchange in their calculation of fair price at settlement on the day (or on the previous day's settlement). Comparing the implied volatility from the previous day's settlement price to the implied volatility of the current price (bid or offer) may give you some measure of the fairness of the quoted price (if there is no perceived change in future volatility). What such a comparison will do is to give you a measure of the degree to which the current market's perception of future volatility has changed over the course of the trading day.

So, specific to your question, you do not want to use an annualised measure. The best you can do is compare the implied volatility in the current price to the implied volatility of the previous day's settlement price while at the same time making a subjective judgement about how you see volatility changing in the future and how this has been reflected in the current price.

The answer by not-nick is wrong. At least for major exchanges like the CME (maybe there are some small exchanges with little option trading that use historical vol, but I would be very surprised).

The CME group (CME, CBOT, NYMEX & COMEX) explains option settlement on the website:

Once the underlying futures have been settled the implied volatility skews will be used in conjunction with the futures settlement price to derive settlement prices for the options.

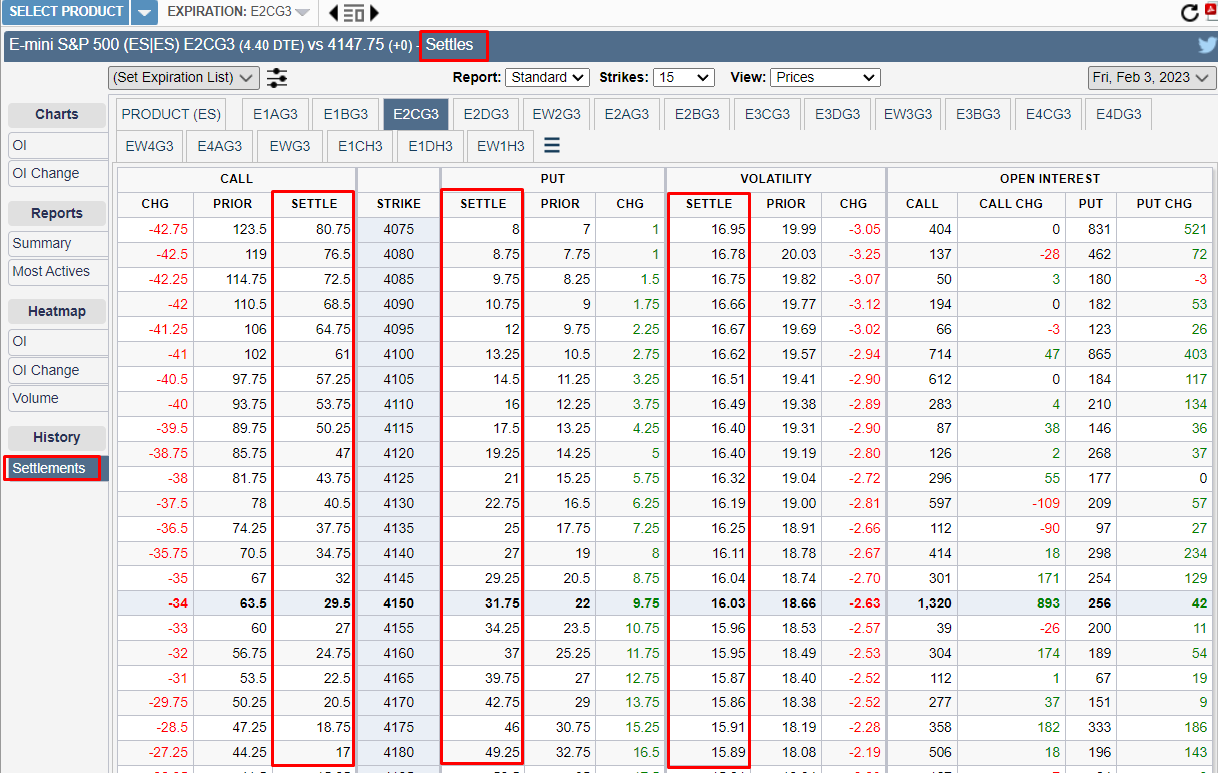

The CME also has a settlement price tool. As you can see below, settlement prices use different IV for the same expiry but different strikes.

It also makes no sense to use historical vol because:

Empirically, IV tends to overestimate RV, commonly referred to as Volatility Risk Premium

IV is the only free parameter in the Black-Scholes-Merton (BSM) model. Higher IV can be a result of compensation for tail risk.

This answer shows how implied vol quotes correct for the flat vol / normal distribution of returns assumption in Black Scholes. The figure below is from the answer.

A few observations:

- increasing ATM vol moves the vol surface up, and spreads out the RN probability distribution

- increasing kurtosis moves the tails out significantly

- a negative RR (higher OTM put vs OTM call IV) increases the left tail, a positive RR the right tail

Since markets frequently have very pronounced skews in the IV surface, and historical vol underestimates implied vol on average, it is completely misleading to rely on historical vol when trying to assess option prices.

If you have listed markets that are price quoted, you can only build a vol surface (which is actually very difficult). The linked answer also shows how for example SVI can be used. It omits lots of details. This answer on quant stack exchange outlines some details for vol surface creation for American options on stocks.

To give you an example that using historical vol makes no sense: Tesla is currently (at close, February 3 04:00PM EST) valued at ~189. According to Yahoo finance, the IV for Tesla for an at the money option is ~ 73.

For strikes around 90, you get the following prices and IVs

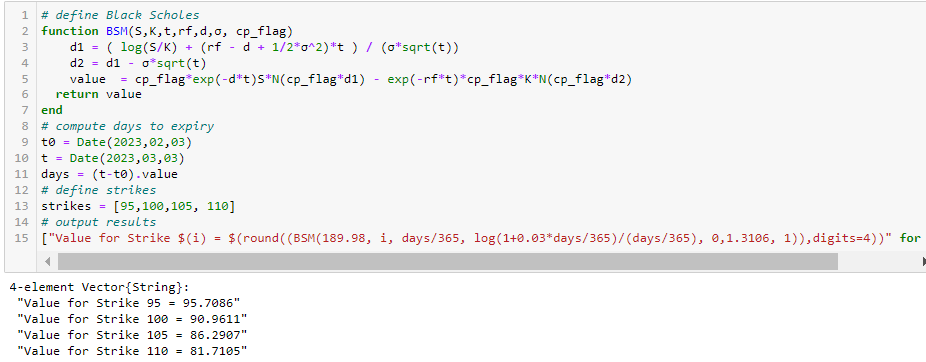

It is quick to check with a coding language or spreadsheet that the values for IV match the price of the option. I'll use Julia below.

# define Black Scholes

function BSM(S,K,t,rf,d,σ, cp_flag)

d1 = ( log(S/K) + (rf - d + 1/2*σ^2)*t ) / (σ*sqrt(t))

d2 = d1 - σ*sqrt(t)

value = cp_flag*exp(-d*t)S*N(cp_flag*d1) - exp(-rf*t)*cp_flag*K*N(cp_flag*d2)

return value

end

# compute days to expiry

t0 = Date(2023,02,03)

t = Date(2023,03,03)

days = (t-t0).value

# define strikes

strikes = [95,100,105, 110]

# output results

["Value for Strike $(i) = $(round((BSM(189.98, i, days/365, log(1+0.03*days/365)/(days/365), 0,1.3106, 1)),digits=4))" for i in strikes]

This pretty much matches the quotes exactly, despite there being after hours trading and different times when the quotes arrived. I chose Tesla because it currently is under a bit of pressure has a pronounced skew.

Edit

Settlement prices are needed for daily mark to market. Futures and options on exchanges are subject to margin requirements. An example with futures is shown here (that is also why the same futures contract has a different price every day). In theory, one could simply use the last traded price for example, but the problem with this is that prices tend to be erratic around the close, and you create room for potential manipulation, if you simply were to use one single price. Therefore, settlement prices are computed.

The model used to compute margin requirement itself also uses historical vol (and IV …). However, that is unrelated to the settlement price. It simple computes the required margin for the product. Option pricing always refers to implied vol and not historical vol.

-

What are they actually settling here? Is it just valuing positions for margin calls or are they actually using these numbers to price real trades somehow? I had assumed that buy/sell prices are a matter for the market participants and the exchange would just deal with settlement at expiry at which point vol should be irrelevant (?) Commented Feb 4, 2023 at 11:54