So, from what I understand:

- APR: rate advertised to borrowers (without compounding)

- APY: rate advertised to lenders (with compounding)

So, for a loan with APR of 6%, that compounds monthly:

- APY = (1 + (0.06/12)) ** 12 - 1 = 6.18%

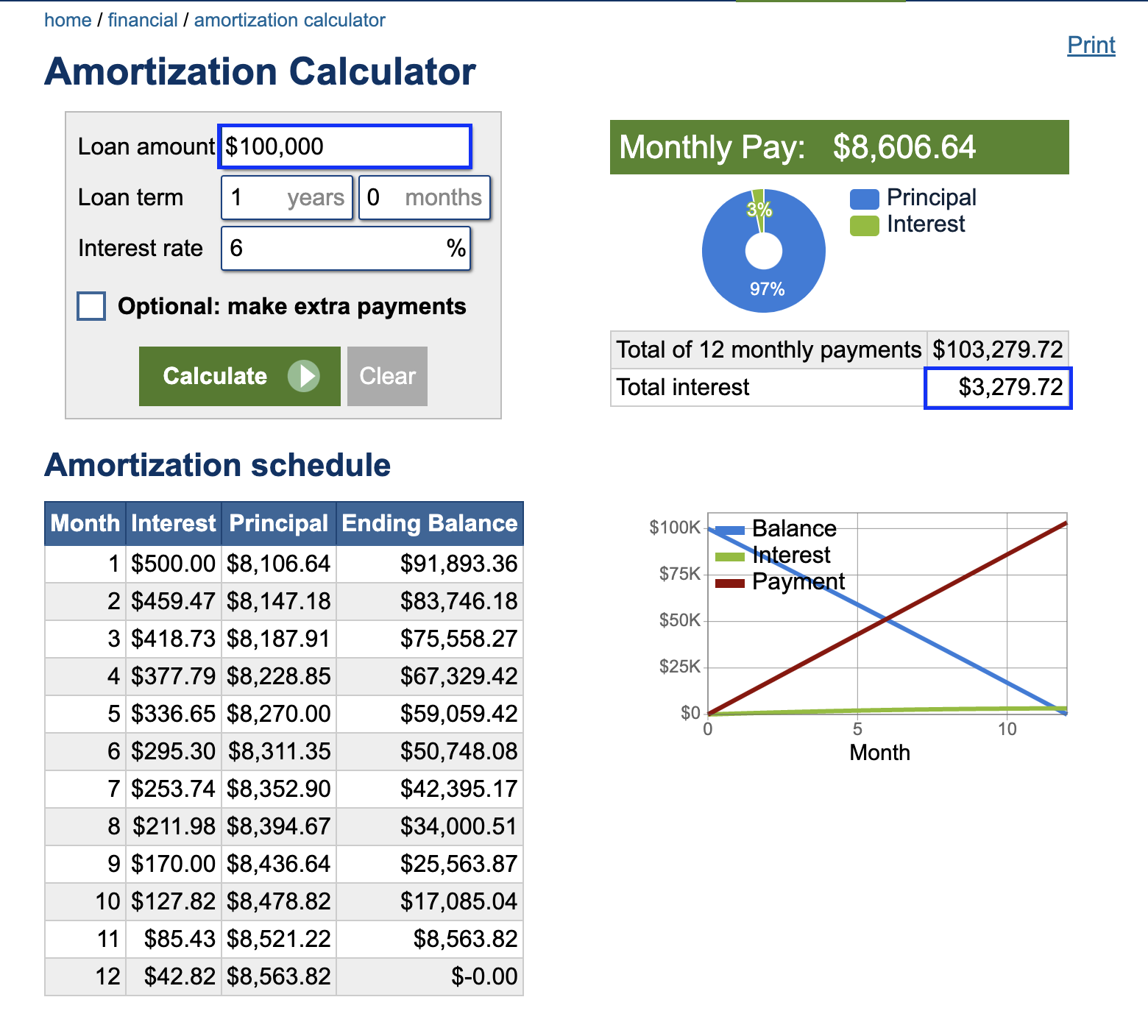

However, let's now put these numbers in an Amortization Calculator:

Now if I'm a Lender, my APY would be total interest / loan amount, right?

Well, if I do:

- 3,279.72 / 100,000.00 = 3.28% (which is lower than 6.18%)

Why is this lower?

- Does the APY for amortization schedules work differently (because interest is front-loaded or whatever)? But since the loan only lasts one year, how would that even make a difference?

- How would things change if the loan lasted say, 5 years?