Problem

How to calculate Effective Annual Interest Rate (EAR) and Annual Percentage Rate (APR) with fees (in R) ?

I am interested in getting to know how much I am actually paying interest when fees are taken into account and I assume EAR is the way to go, but correct me if I am wrong.

I tried to implement APR below as in the investopedia description but APR is lower than nominal interest so it is certainly not correct (should be around 3.5%)

What I have tried

Below an MVE which also explains the problem in more detail:

rm(list=ls())

library(reprex)

# define costs, fees and interests

price <- 24800

monthly_payment <- 280

deposit <- 4000

loan_term <- 5*12 #in months

initial_fee <- 300

monthly_fee <- 12

nominal_interest <- 2/100

monthly_interest <- nominal_interest/12

# initiate fixed costs, interest fees and total costs for the loop

handling_charges <- initial_fee

interest_fees <- 0

total_costs <- handling_charges

# substracting initial payment from the what is left variable

left <- price - deposit

#calculating how much of dept is left after loan period and how much interest has accumulated

for (i in 1:loan_term) {

left_last_month <- left

left <- left*(1+monthly_interest)

interest_fees_mo <- (left-left_last_month)

interest_fees <- interest_fees + interest_fees_mo

handling_charges <- handling_charges + monthly_fee

total_costs <- total_costs+ interest_fees_mo + monthly_fee

left <- left+monthly_fee-monthly_payment

}

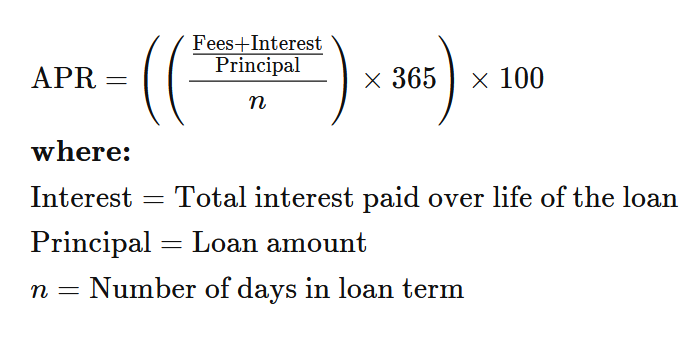

#https://www.investopedia.com/terms/a/apr.asp

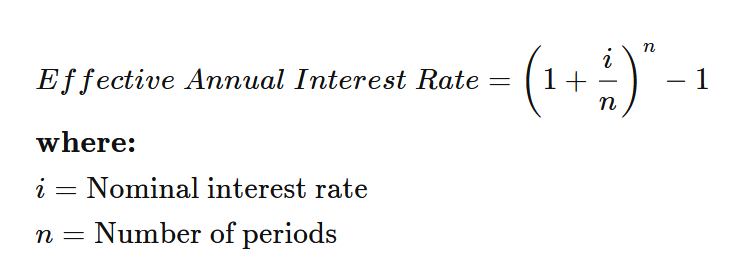

#https://www.investopedia.com/terms/e/effectiveinterest.asp

apr_100 <-

((

(total_costs/price)

/(loan_term*30.4375) # number of days in the loan term

)

*365.25) # number of days in a year

apr <- apr_100*100

# ear ???

share_of_loan_100 <- (total_costs/price)*100

share_of_loan_100

#> [1] 9.632864

left # after loan period ends

#> [1] 6088.95

interest_fees

#> [1] 1368.95

handling_charges

#> [1] 1020

total_costs

#> [1] 2388.95

apr # wrong

#> [1] 1.926573

# ear # ????

Created on 2022-01-20 by the reprex package (v2.0.1)

Definitions from investopedia:

APR

EAR, no fees taken into account

EDIT2:

Based on base64's suggestions, I think it is working now, albeit the code is ugly. Do you think it now give correct apr & apy ?

I added an option to either predifine monthly payment or calculate it based on the final payment (by setting monthly payment to FALSE, it will be approximated). There is also an option to choose when the interest compounds (eg. 1:12 for monthly, 1 for the first month of the year, c(6,12) for the 6th and 12th month of the year, since the beginning of the loan period).

After running the code, you can just plug in the values in the interest.F-function. See the two examples at the end (stack_example_monthly & stack_example_annual)

rm(list=ls())

library(reprex)

library(gtools)

# We need 3 helper functions

# 1. a precise enough binary search function

# 2. Payments function to calculate payments during the loan period

# 3. Apr to calculate the real interest rate

##########################################################

# 1. Binary search - helper function

##########################################################

# gtools binsearch-function modified for more accurate search results

# source: Gregory R. Warnes, Ben Bolker and Thomas Lumley (2021). gtools: Various R Programming Tools. R package version 3.9.2. https://CRAN.R-project.org/package=gtools

binsearch_decimal <- function(fun, range, ..., target = 0, lower = ceiling(min(range)),

upper = floor(max(range)), maxiter = 1000, showiter =FALSE)

{

lo <- lower

hi <- upper

counter <- 0

val.lo <- fun(lo, ...)

val.hi <- fun(hi, ...)

if (val.lo > val.hi) {

sign <- -1

}

else {

sign <- 1

}

if (target * sign < val.lo * sign) {

outside.range <- TRUE

}

else if (target * sign > val.hi * sign) {

outside.range <- TRUE

}

else {

outside.range <- FALSE

}

while (counter < maxiter && !outside.range) {

counter <- counter + 1

if (hi - lo <= 0.00001 || lo < lower || hi > upper) # 1 -> 0.00001

break

center <- round((hi - lo)/2 + lo, 6) # 0 -> 6

val <- fun(center, ...)

if (showiter) {

cat("--------------\n")

cat("Iteration #", counter, "\n")

cat("lo=", lo, "\n")

cat("hi=", hi, "\n")

cat("center=", center, "\n")

cat("fun(lo)=", val.lo, "\n")

cat("fun(hi)=", val.hi, "\n")

cat("fun(center)=", val, "\n")

}

if (val == target) {

val.lo <- val.hi <- val

lo <- hi <- center

break

}

else if (sign * val < sign * target) {

lo <- center

val.lo <- val

}

else {

hi <- center

val.hi <- val

}

if (showiter) {

cat("new lo=", lo, "\n")

cat("new hi=", hi, "\n")

cat("--------------\n")

}

}

retval <- list()

retval$call <- match.call()

retval$numiter <- counter

if (outside.range) {

if (target * sign < val.lo * sign) {

warning("Reached lower boundary")

retval$flag <- "Lower Boundary"

retval$where <- lo

retval$value <- val.lo

}

else {

warning("Reached upper boundary")

retval$flag <- "Upper Boundary"

retval$where <- hi

retval$value <- val.hi

}

}

else if (counter >= maxiter) {

warning("Maximum number of iterations reached")

retval$flag <- "Maximum number of iterations reached"

retval$where <- c(lo, hi)

retval$value <- c(val.lo, val.hi)

}

else if (val.lo == target) {

retval$flag <- "Found"

retval$where <- lo

retval$value <- val.lo

}

else if (val.hi == target) {

retval$flag <- "Found"

retval$where <- hi

retval$value <- val.hi

}

else {

retval$flag <- "Between Elements"

retval$where <- c(lo, hi)

retval$value <- c(val.lo, val.hi)

}

return(retval)

}

##############################################3

# 2.payments - helper function

##############################################

#calculating how much of dept is left after loan period and how much interest has accumulated

# includes an option to calculate monthly payment with binary search

payments.F <- function(monthly_payment, #

binary_search,

monthly_fee, #

nominal_interest,

price, #

deposit, #

initial_fee,

loan_term,

compounding) {#

# substracting initial payment and initial fees to get principal

principal <- price - deposit

left <- principal

# initiate parameters for the loop

handling_charges <- initial_fee

interest_fees <- 0

total_costs <- handling_charges

monthly_interest <- nominal_interest/12

month <- 1

no_of_compoundings <- length(compounding)

compounding_period_interest <- nominal_interest/length(compounding)

#defining a "not in" operator

`%!in%` <- Negate(`%in%`)

if ( (sum(compounding %in% 1:12) >0) & (sum(compounding %!in% 1:12) ==0) ) {

#print('--a valid compounding period set--')

} else {

stop("Error: Invalid compoumding value. Set it to a vector of months when you want it to compound, e.g. 1:12, c(6,12),5")

}

for (i in 1:loan_term) {

left_last_month <- left

if (month %in% compounding) {

left <-left*(1+compounding_period_interest)

}

interest_fees_mo <- (left-left_last_month)

interest_fees <- interest_fees + interest_fees_mo

handling_charges <- handling_charges + monthly_fee

total_costs <- total_costs+ interest_fees_mo + monthly_fee

left <- left+monthly_fee-monthly_payment

# incrementing or resetting monthly counter

month <- month+1

if (i %% 12 == 0) {

month <- 1

}

}

if (binary_search==T) {

return(left)

} else {

return(list("principal"=principal,

"left"=left,

"total_costs"=total_costs,

"interest_fees"=interest_fees,

"handling_charges"=handling_charges

))

}

}

############################################################################

# 3. APR - helper function

############################################################################

#apr will be later solved with binary search

apr.F <- function(APR,PMT,N,FV,PV) {

(PMT*((1-(1/(1+(APR/12))^N))/(APR/12)))+(FV/(1+(APR/12))^N)-(PV)

}

###########################################################################

# main function where we plug in the values

interest.F <- function(price,

loan_term=5*12,

initial_fee=0,

nominal_interest=2/100,

monthly_fee=12,

deposit=4000,

monthly_payment=F, # Set to false if you want to calculate monthly payment

final_payment=0, # If monthly payment is set, it will overrun this

compounding=1:12

) {

# running binary search to monthly cost if we have not defined it

if (monthly_payment==F) {

print('--Calculating monthly payment by binary search--')

(binsearch_monthly_payment <- binsearch_decimal(function(x)

payments.F(x, #

binary_search=T,

monthly_fee=monthly_fee, #

nominal_interest=nominal_interest,

price=price, #

deposit=deposit, #

initial_fee=initial_fee,

loan_term=loan_term,

compounding=compounding),

range = c(0,2000),

target=final_payment,

showiter = F))

monthly_payment <- mean(binsearch_monthly_payment$where)

} else {

print('--Using pre-fixed monthly payment amount--')

}

# assigning a payment scheme based on monthly payment (binary search or predefined)

(payments <- payments.F(monthly_payment,

binary_search = F,

monthly_fee=monthly_fee, #

nominal_interest=nominal_interest,

price=price, #

deposit=deposit, #

initial_fee=initial_fee,

loan_term=loan_term,

compounding=compounding))

paid_excluding_fees <- payments$principal-payments$left

# running a binary search to find apr given that we know how much we have repayed the loan (excluding fees)

(binsearch_apr <- binsearch_decimal(function(x)

apr.F(x,

PMT=monthly_payment,

N=loan_term,

FV=payments$left,

PV=payments$principal-initial_fee)

, range = c(-1,100),target=0))

#taking the mean value of the binary search to approximate apr

apr <- mean(binsearch_apr$where)

apr <- apr

#calculating apy based on apr

#https://www.investopedia.com/terms/a/apy.asp

apy <- (1+apr/12)^12-1

share_of_price <- (payments$total_costs/(price-initial_fee))*100

#payments$paid_excluding_fees <- paid_excluding_fees

payments$all_payments <- payments$total_costs + paid_excluding_fees +deposit

payments$monthly_payments <- monthly_payment

payments$share_of_price <- share_of_price

payments$apr <- apr*100

payments$apy <- apy*100

return(payments)

}

(stack_example_monthly <- interest.F(

price=24800,

loan_term=5*12,

initial_fee=300,

nominal_interest=2/100,

monthly_fee=12,

deposit=4000,

monthly_payment=F, # 280 # Set to false to estimate monthly payment

final_payment=6088.95, # 6088.95 If monthly payment is set, it will overrun this

compounding=1:12 # a vector, eg. 1:12, c(6,12), 5.

))

#> [1] "--Calculating monthly payment by binary search--"

#> $principal

#> [1] 20800

#>

#> $left

#> [1] 6088.95

#>

#> $total_costs

#> [1] 2388.95

#>

#> $interest_fees

#> [1] 1368.95

#>

#> $handling_charges

#> [1] 1020

#>

#> $all_payments

#> [1] 21100

#>

#> $monthly_payments

#> [1] 280

#>

#> $share_of_price

#> [1] 9.750817

#>

#> $apr

#> [1] 3.5069

#>

#> $apy

#> [1] 3.56382

(stack_example_annual <- interest.F(

price=24800,

loan_term=5*12,

initial_fee=300,

nominal_interest=2/100,

monthly_fee=12,

deposit=4000,

monthly_payment=280, # 280 # Set to false to estimate monthly payment

final_payment=NA, # 6088.95 If monthly payment is set, it will overrun this

compounding=12 # a vector, eg. 1:12, c(6,12), 5.

))

#> [1] "--Using pre-fixed monthly payment amount--"

#> $principal

#> [1] 20800

#>

#> $left

#> [1] 5921.857

#>

#> $total_costs

#> [1] 2221.857

#>

#> $interest_fees

#> [1] 1201.857

#>

#> $handling_charges

#> [1] 1020

#>

#> $all_payments

#> [1] 21100

#>

#> $monthly_payments

#> [1] 280

#>

#> $share_of_price

#> [1] 9.068805

#>

#> $apr

#> [1] 3.2841

#>

#> $apy

#> [1] 3.333986

Created on 2022-02-13 by the reprex package (v2.0.1)

{kind=link}