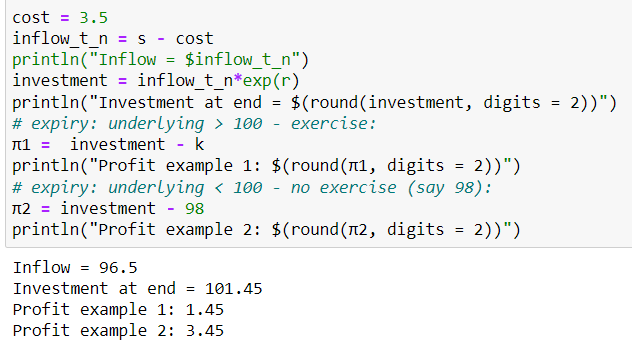

- Suppose that the current stock price is €100, the exercise price is €100, the annually compounded interest rate is 5 percent, the stock pays a €1 dividend in the next instant, and the quoted call price is €3.50 for a one year option. Identify the appropriate arbitrage opportunity and show the appropriate arbitrage strategy.

My attempted answer:

Early Exercise of American Calls on Dividend-Paying Stocks

When a company declares a dividend, it specifies that the dividend is payable to all stockholders as of a certain date, called the holder-of-record date. Two business days before the holder-of-record date is the ex-dividend date. To be the stockholder of record by the holder-of-record date, one must buy the stock by the ex-dividend date. The stock price tends to fall by the amount of the dividend on the ex-dividend date.

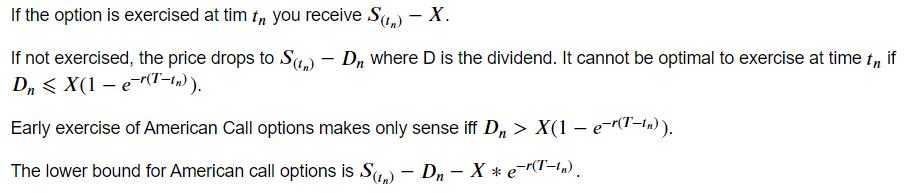

When a stock goes ex-dividend, the call price drops along with it. The amount by which the call price falls cannot be determined at this point in our understanding of option pricing. Since the call is a means of obtaining the stock, however, its price could never change by more than the stock price change. Thus, the call price will fall by no more than the dividend. An investor could avoid this loss in value by exercising the option immediately before the stock goes ex-dividend. This is the only time the call should be exercised early.

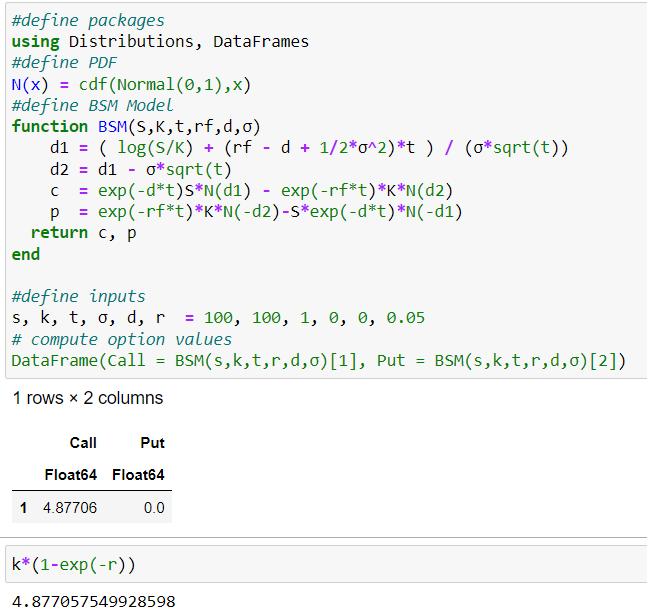

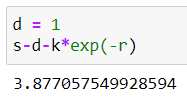

Another way to see that early exercise could occur is to recall that we stated that the lower bound of a European call on a dividendpaying stock is Max [itex][ 0, S'_0 - X(1 + 0.05)^-1][/itex] where $S'_0$ is the stock price minus the present value of dividends. X is the strike price $$100$. To keep things simple, assume only one dividend of the amount D, and that the stock will go ex-dividend in the next instant. Then $S'_0$ is approximately equal to $S_0 -D= $100-$1= $99 $ (since the present value of D is almost D). Since we would consider exercising only at-the-money call, assume that $S_0= $100 $ equals $X($100)$. Then it is easy to see that $S_0 - X= $100-$100 = 0$ could not exceed $S'_0 - X(1+0.05)^-1= $100 - $100(1+0.05)^-1= $3.76 $. By exercising the option, the call holder obtains the value $S_0 -X =$100 -$100= 0 $

Visit here for neat, legible

[Answer]

[1]https://quant.stackexchange.com/q/74236/15605