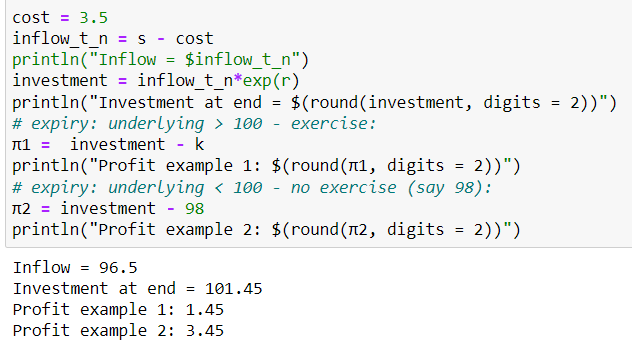

However, 3.5 < 3.87, in which case the call option is less than the theoretical minimum. An arbitrageur can buy the call and short the stock, to get a cashflow equal to the proceeds of the stock minus the cost of the call. Invested at the prevailing one-year interest rate, you can get a certain payoff at the end of the year, where the option expires. If the stock price is above the strike price, the arbitrageur exercises the option, closes out the short position and makes a profit equal to the difference between spotsthe investment and strike.

You are confusing a lot of things here. The question (homework?) does not discuss early exercise of American options but is simply about arbitrage.

With regards to early exercise:

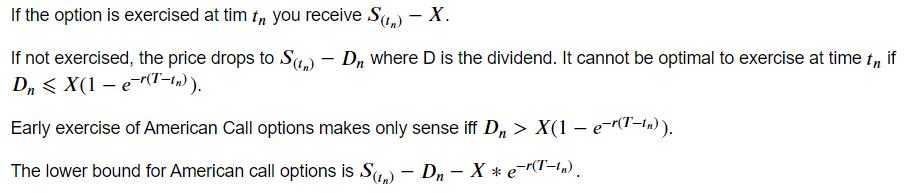

If the option is exercised at tim t_n you receive S_(t_n)= - X. That would already be sufficient because in your example S = X = 100 and you will get 0. Getting zero for something that is not worthless (quoted price of 3.5) is suboptimal.

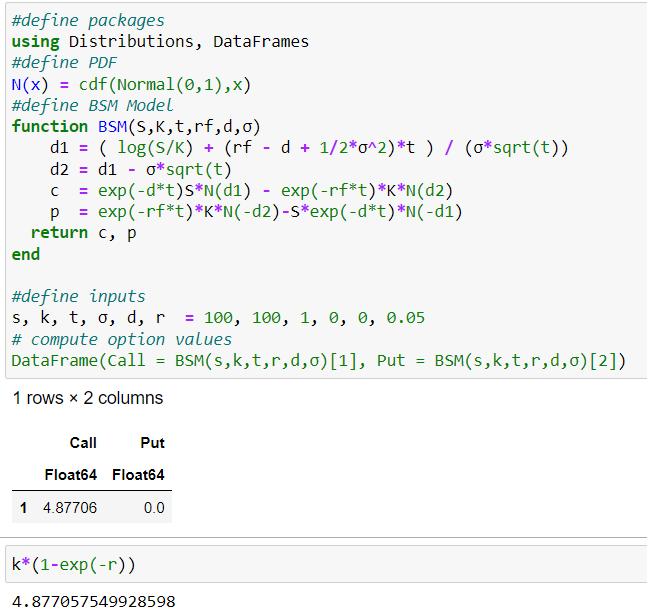

If not exercised, the price drops to S_(t_n) - D_n where D is the dividend. More generally, it is straightforward to show that it cannot be optimal to exercise at time t_n if D_n ⩽ X(1-e^{-r(T-t_n)}). It is not a coincidence that X(1-e(-0.05)) ≈ 4.88 which was your deleted Black Scholes pricing screenshot, because you had zero volatility and no dividends, in which case you do not need an option pricing model. This is also quick to verify with a bit of code (Julia).

#define packages

using Distributions, DataFrames

#define PDF

N(x) = cdf(Normal(0,1),x)

#define BSM Model

function BSM(S,K,t,rf,d,σ)

d1 = ( log(S/K) + (rf - d + 1/2*σ^2)*t ) / (σ*sqrt(t))

d2 = d1 - σ*sqrt(t)

c = exp(-d*t)S*N(d1) - exp(-rf*t)*K*N(d2)

p = exp(-rf*t)*K*N(-d2)-S*exp(-d*t)*N(-d1)

return c, p

end

#define inputs

s, k, t, σ, d, r = 100, 100, 1, 0, 0, 0.05

# compute option values

DataFrame(Call = BSM(s,k,t,r,d,σ)[1], Put = BSM(s,k,t,r,d,σ)[2])

Early exercise of American Call options makes only sense iff D_n > X(1-e(-r)).

Arbitrage

You do have, as the question suggests, arbitrage though. Since I assume it is homework, I will only hint the result.

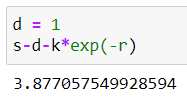

The lower bound for American call options is S_(t_n)-D_n - X*exp^{-r(T-t_n)}.

However, 3.5 < 3.87, in which case the call option is less than the theoretical minimum. An arbitrageur can buy the call and short the stock, to get a cashflow equal to the proceeds of the stock minus the cost of the call. Invested at the prevailing one-year interest rate, you can get a certain payoff at the end of the year, where the option expires. If the stock price is above the strike price, the arbitrageur exercises the option, closes out the short position and makes a profit equal to the difference between spot and strike.

If the stock is less than strike, the stock is bought in the market and the short position is closed out - this will yield an even greater profit.

Any introductory option pricing book like Hull explains this in more detail.

Apologies notation wise, but Money stackexchange does not support Latex.

A numerical example in code: