I want to buy an option on NCLH. One option is June 2021, strike price=25 and the other one is Jan. 2022, strike price=27.5. Consider the speed of cruise recovery, which option is better?

Add a comment

|

1 Answer

The short answer is that it will depend on how much NCLH rises, when it occurs and how much implied volatility changes.

A more complex answer is that if you set this up as a diagonal spread in a pricing model (buy the 2022 call and sell the 2021 call), the graph will show you the performance.

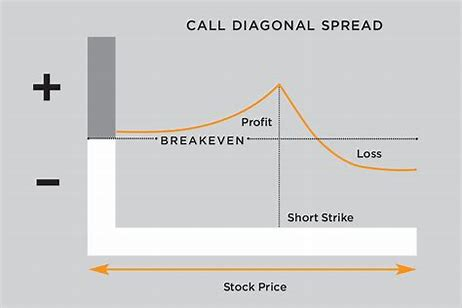

Here's an expiration diagram of a call diagonal:

Note that the position makes money initially. This is because the theta of the $27.50 call is lower and initially, it's delta is higher. At some point, the delta reverses and the $25 call becomes stronger and the profit line starts dropping. The inflection point would be around $25. IOW, the $27.50 call does better initially and the $25 call does better later.

Prior to expiration. it's never that simple because of option pricing behavior. I don't know of an online resource that provides pre-expiration with time slices but if you grasp the concept of using the diagonal spread as a proxy and since I'm not adept at uploading images, all I can offer is this somewhat cruder way of visualizing this. Set up the spread there and you'll see the appropriate numbers.

answered Nov 10, 2020 at 1:17