The main reason to limit employee's 401k contributions is because the IRS imposes limits. It's not the employer making that decision, it's the government.

The government has an obvious reason to limit contributions: They reduce tax revenue. The government has decided that it wants to encourage and facilitate people saving for retirement, but it puts limits on this to prevent people from taking advantage of the rules and using it for other purposes, or from getting an "unfair" tax advantage.

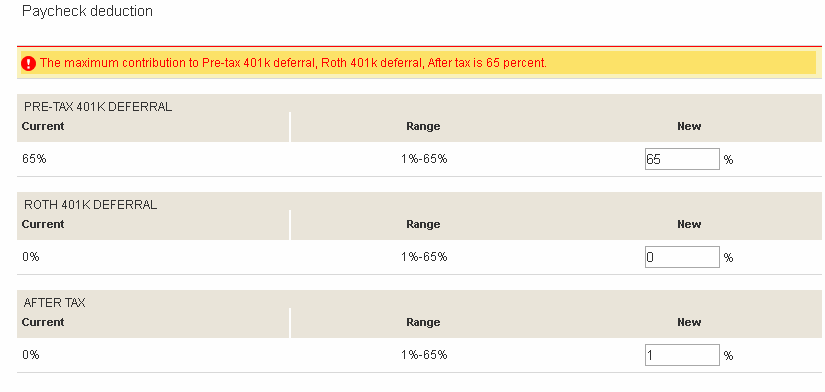

There are also "non-discrimination" rules intended to prevent a company from setting up a retirement plan that benefits only the owner and maybe a few top executives. So if too high a percentage of the money in a plan is coming from high-paid employees, the company has to impose extra limits to balance it. These rules are fairly complex.

That said, I am not aware of any 65% rule. The government limits on 401k contributions are: $18,500 per year ($24,500 if you're over 50), or 100% of your gross income, whichever is less. It's possible that this is part of a scheme to comply with the non-discrimination rules.

In any case, do you really want to put over 65% of your income toward retirement? What will you live on? Great if you can manage it, but you've got to be a rare case. I suppose there might be some number of two income household that could live on one person's income and put most or all of the other person's toward retirement.