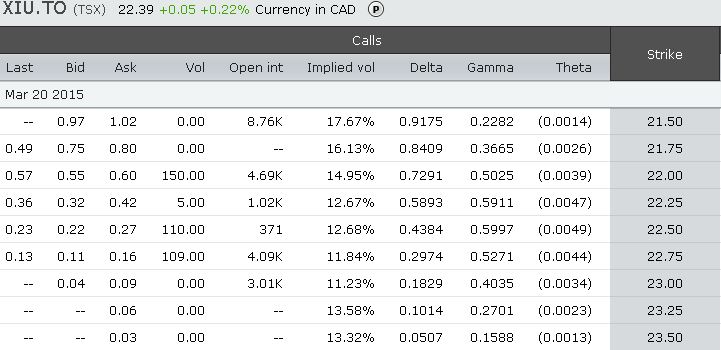

I understand that ITM have little time value, so they will have small time decay(theta), but why OTM has a lesser theta than ATM?

The Time value represents uncertainty. That uncertainty decreases the farther away from ATM you get (in either direction). At-the-money, there is roughly a 50% chance that the option expires worthless. As you get deeper in-the-money, the change that is expires worthless decreases, so there is less uncertainty (there is more certainty that the option will pay off). As you go deeper OTM, the probability that the option expires worthless increases, so there is also less uncertainty.

At the TTM decreases, the uncertainty (theta) decreases as well, since there is less time for the option to cross the strike from either direction. Similarly, as volatility decreases, theta decreases, since low-volatility stocks have a less change of crossing the strike.