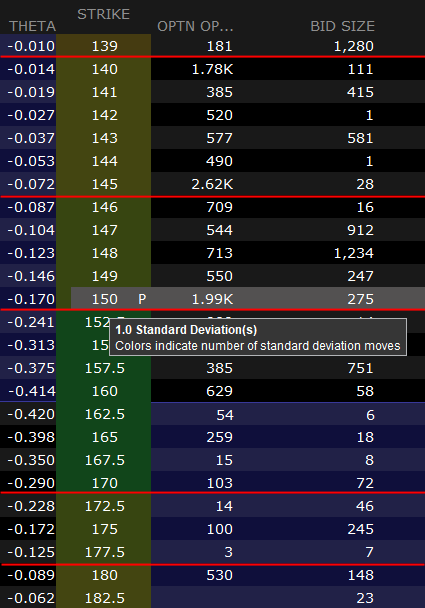

I originally posted this question to the coding section of StackOverflow, but did not receive any replies. I am wanting to calculate the min and max values for the various standard deviation "groups" similar to those as displayed in the Interactive Brokers Trader WorkStation (TWS) for option chains, i.e.:

In the screen snapshot above the strike prices are grouped by color to indicate the number of standard deviation moves (I added the red lines to separate the color groups).

I would like to know how the min and max values in each group are calculated.

I was hoping someone could shed some light on how these numbers are calculated or provide a step-by-step formula or resource for doing so.

Update:

Thank-you @D Stanley.

The API I am using provides option Greeks for various tick types, for example, the following values were obtained from the API (different option chain from the one shown in screenshot above):

Stock last price: 33.01

Option Model underlying price: 32.86088562011719

Option Model Implied Volatility: 2.397441799226127

1SD = Option Model underlying price * Option Model IV * SQRT( days_to_expiration / trading_days_per_year )

= 32.86088562011719 * 2.397441799226127 * SQRT( 4 / 256 );

= 9.847757593157215

I can then calculate the min/max price range using the 1SD value, i.e:

price_min = Option Model underlying price - 1SD

= 32.86088562011719 - 9.847757593157215

price_max = Option Model underlying price + 1SD

= 32.86088562011719 + 9.847757593157215

I used a value of 256 from a reference book (Option Volatility & Pricing).

But I still have my doubts as to which Implied Volatility one uses as the API returns an IV value for various tick types, i.e.:

TickType.OPTION_IMPLIED_VOL - A prediction of how volatile an underlying will be in the future. The 30-day volatility is the at-market volatility estimated for a maturity thirty calendar days forward of the current trading day and is based on option prices from two consecutive expiration months.

TickType.LAST_OPTION -- Computed Greeks and implied volatility based on the underlying stock price and the option last traded price

TickType.ASK_OPTION -- Computed Greeks and implied volatility based on the underlying stock price and the option ask price ...

TickType.BID_OPTION -- Computed Greeks and implied volatility based on the underlying stock price and the option bid price ...

I was using TickType.OPTION_IMPLIED_VOL values, but I think I should be using TickType.LAST_OPTION values. Also, I am using the underlying (stock) price from the option data returned as well.

Thanks in advance.