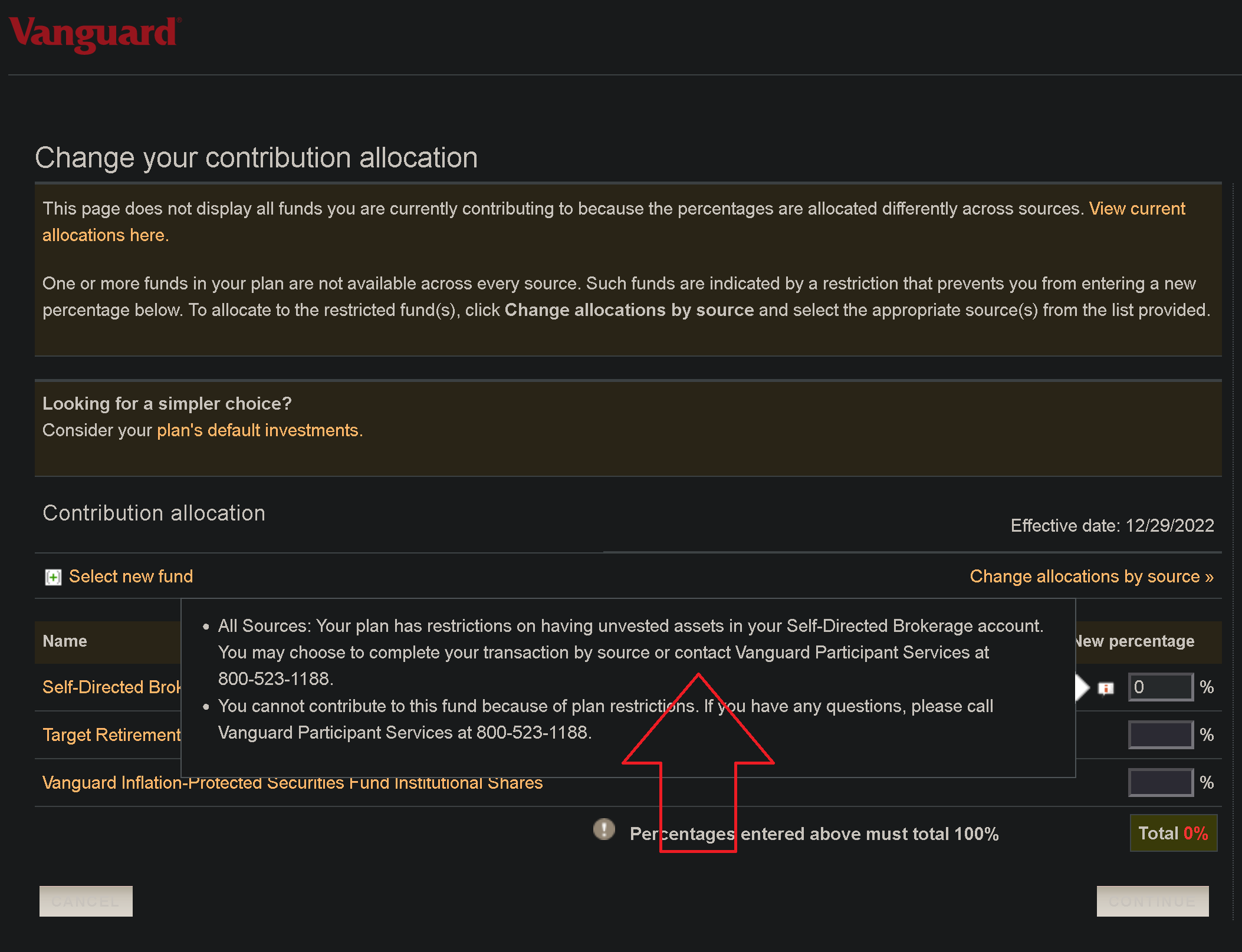

"Unvested" just means that the employer has contributed the amount (on paper, at least) but can claw them back if you terminate employment or for some other reason that would violate the vesting agreement.

For example, If I start a new job and contribute $1,000 with a full match, I "have" 2,000 available to invest, but half of it is "unvested" and I would give it up if I quit. Providers account for these in separate "buckets" that may or may not be visible to you.

So the funds are "in your account" in a manner of speaking (meaning you can invest them, they can earn returns, etc.) but those funds (and any returns associated with them) would be forfeited under certain conditions.

That forfeiture would likely be much more difficult (if not impossible) in a self-directed account where you can contribute to a wider variety of assets, including things like derivatives and real estate (under very strong restrictions). There may also be IRS regulations that I am not aware of (a quick search did not find anything definitive) regarding unvested funds in a self-directed account.