I am sure you must mean "The lender has provided to charge a fixed amount of interest each month", because the interest would be in proportion to the balance owed which decreases as the loan is paid down.

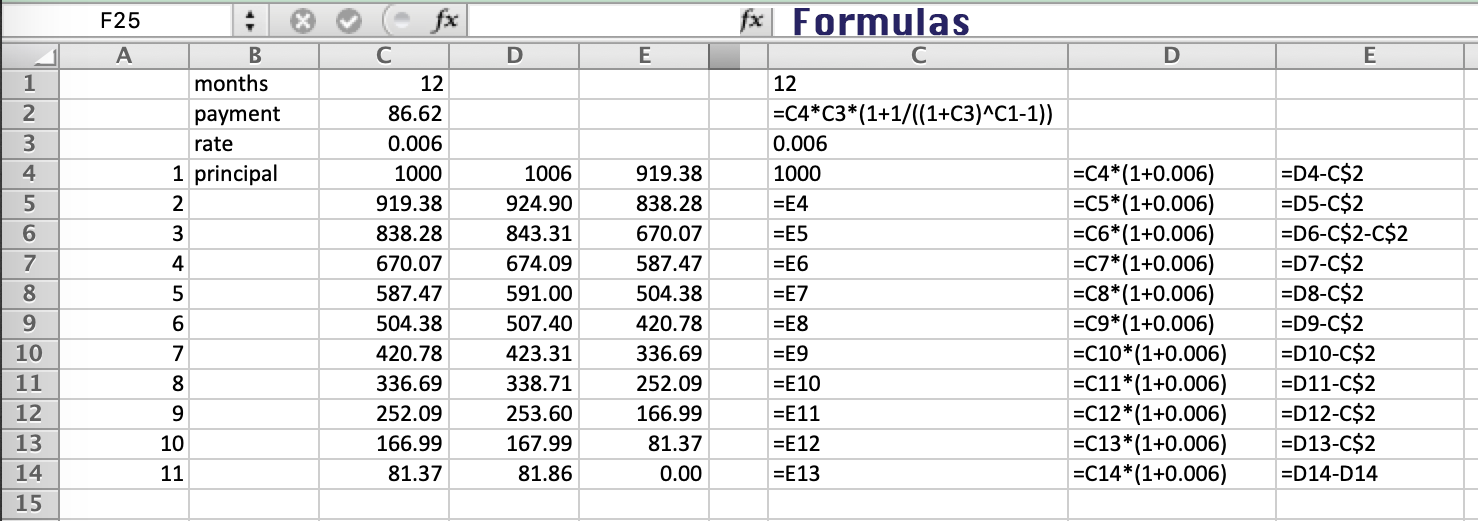

So taking an example of a $1000 loan, with 7.2% nominal annual interest compounded monthly using 30/360 amortised over 12 months.

With

principal s = 1000

annual rate . . 0.072

daily rate . . 0.072/360 = 0.0002

monthly rate r = 0.0002*30 = 0.006

number of months n = 12

monthly payment d = s r (1 + 1/((1 + r)^n - 1)) = 86.62

the fixed payment amount would be $86.62

Case of a double-sized payment

For example, if the borrower makes a double payment in the 3rd payment.

The balance b after a normal 3rd payment (x = 3) would be

x = 3

b = (d + (1 + r)^x (r s - d))/r = 756.69

and you could recalculate the payments from the 3rd month and they would be the same

s = b

r = 0.006

n = 9

d = s r (1 + 1/((1 + r)^n - 1)) = 86.62

or calculating n from s, r & d

n = -(log(1 - (r s)/d)/log(1 + r)) = 9

However, with the double payment the principal s remaining is less

s = b - d = 670.07

r = 0.006

n = 9

d = s r (1 + 1/((1 + r)^n - 1)) = 76.70

and the payment amounts for the remaining 9 months would only be $76.70

Or the payment could be kept at $86.62 and the loan would be paid down sooner: Calculating n

s = b - d = 670.07

r = 0.006

d = 86.62

n = -(log(1 - (r s)/d)/log(1 + r)) = 7.945

The loan would be paid down before 8 further payments. So calculating the balance after the 7th further payment ...

s = b - d = 670.07

r = 0.006

d = 86.62

x = 7

b = (d + (1 + r)^x (r s - d))/r = 81.37

The balance after the 7th further payment is $81.37 and the final payment would be

b (1 + r) = 81.86

The final payment in the 11th month overall would be $81.86

You could do these calculations in Excel, or using a pocket calculator. It is not actually necessary to set up a Excel amortisation table, although it's a good check.

Case of an extra payment on any day

For example, if an extra payment of $100 is made 10 days after the 3rd regular payment.

As above, the balance b after the normal 3rd payment (x = 3) would be

x = 3

b = (d + (1 + r)^x (r s - d))/r = 756.69

After ten days of interest at the daily rate of 0.02%

s = b * (1 + daily rate * 10) = 756.69 * 1.002 = 758.20

Then the $100 extra payment is made

s = s - 100 = 658.20

In order to not reset the payment dates, backtrack 10 days of interest from the new balance and recalculate the payments for the original dates.

s = s/1.002 = 656.89

r = 0.006

n = 9

d = s r (1 + 1/((1 + r)^n - 1)) = 75.19

After the $100 payment the regular payments reduce to $75.19 for the remaining 9 payments.