I want to buy a house but I do not have quite enough for the 20% down payment I'd ideally like to post for the mortgage. My wife and I are thinking of chatting with our family and getting together some funds for a down payment. I was thinking, would it be possible to create some type of joint investment in the purchase of the home? Not just a gift or anything informal but joint ownership with some type of fractional ownership based on the downpayment. Here is what I had in mind:

Scenario One:

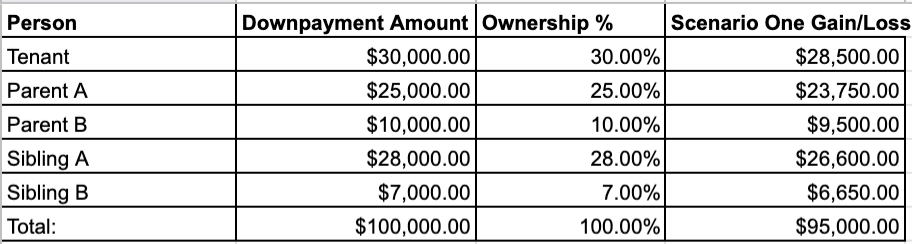

Home Purchase Price = $500,000

Home Sale Price = $600,000

Gain/Loss: $100,000.00

Costs for Closing at 5% $5,000.00

Net Profit $95,000.00

In the scenario above the tenant would be the one living in the property and paying all of the rent (hypothetically) for the privilege of earning a profit on their home when they'd otherwise be renting. Also, as they are owning they have an incentive to take care of the home as well to retain resale value. Let's ignore what would happen if the property were to be rented to someone other than the tenant for the time being.

I am interested in if any legal structures come to mind, if this is already done somewhere at scale, or whether there are U.S. or state regulations preventing this. For reference, this would be in the state of Illinois, Florida, New York, or anywhere in the U.S. ultimately. Of course, please let me know if something does not add up above.