No, it won't affect your score until your statement is posted. Paying your bill before your statement is posted is actually a good way to keep your credit utilization low. If you're worried about high credit utilization negatively affecting your credit score, consider paying your bill several times a month to ensure that when your final monthly statement is posted, your utilization is still low. When my credit limit was very low while I was in college, I did this almost every month, and I've seen other sites recommend this practice as well.

From creditkarma.com:

The easiest way [to lower credit utilization] is to make credit card payments more than once a month so that your balance never gets too high.

and creditcards.com:

Consider making payments to creditors more than once each month. Otherwise, if you put a major expense -- like a new appliance -- on a credit card, even if you plan to pay it off, your FICO score may take a hit. The reason is that credit scores are calculated as a snapshot in time, so if that happens to be right after you charged a new $700 washing machine, your utilization ratio will look worryingly high.

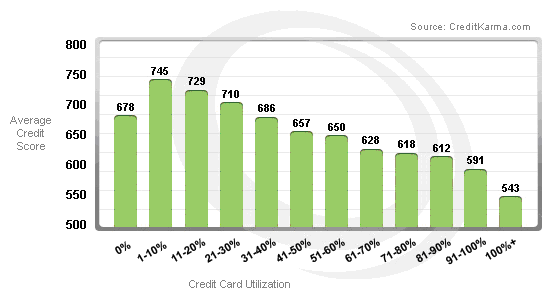

Remember, though, that it's best to have some balance on your card when your statement is posted (assuming you pay it off in full each month), because as the chart shows, 0% utilization is about as bad as utilization > 31-40%:

Also, remember that credit utilization affects your credit score in real time, so if you have high utilization one month but a lower utilization the next month, the hit to your score will disappear once a statement with low utilization is posted.