I just got approved for a $1500 cash secured credit card from Wells Fargo.

This means I have no credit history whatsoever, and am going to use this card to establish one.

With fall semester at school already in full swing, I need to pay for my $1200 health insurance by next week.

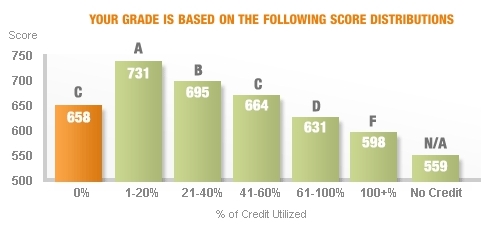

I am thinking of paying for my car and health insurance, both using this credit card, but that would bring my utilization to 100% - maybe a few bucks left at the most.

Now, this scenario would happen, if you guys recommend me to go ahead with it, once a year, when I need to pay for both.

The remaining time of the year, my utilization would be 30% at most.

How bad would hitting the credit limit affect my growth of credit history and score?

Should I go ahead and max out my secured credit card, once a year?

I already have the money in my CU's checking account, and they pay 1.15% on it.

If maxing out is really a very bad idea, I can go ahead and pay the money using my debit card.