In the long run, yes. In the short term, no.

Having more accounts and higher total credit limit is a good thing. From the potential lender's perspective, someone else has apparently reviewed your profile in the past and decided that you were creditworthy.

However, building credit account numbers should be a gradual process, just like accumulating the credit history. If you apply for quite a few credit cards in a very short period of time, it would look really bad to lenders because it makes you look desperate and risky. Unless of course you don't have an immediate need for credit and would simply like to focus on building credit history along with account numbers.

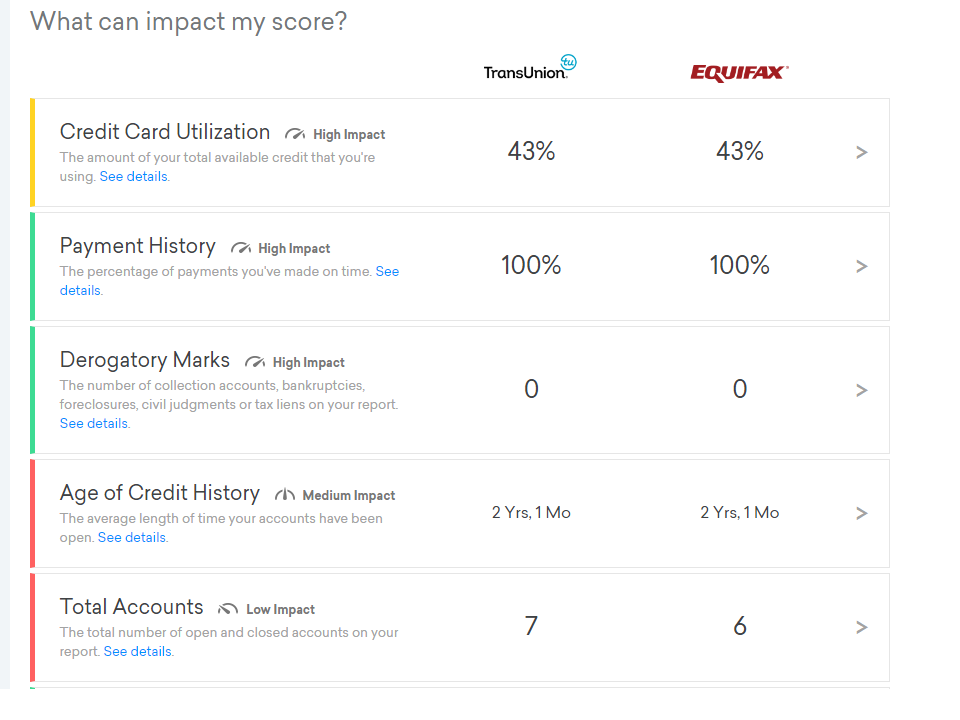

In your situation, since you have a need for credit and would like to see a better score in the short term, the most effective approach is simply to reduce your credit utilization. You would notice that total account number has a low impact on your credit score, but credit utilization has a high impact. Pay off your credit card balances in full if you can, and you will see that score taking off.

EDIT:

(Per @Mindwin's suggestion) here is how applying for/opening new accounts shortly before seeking approval of a new loan hurts you.

1. Multiple hard inquiries

The list in the screenshot you posted from CK website should also include another item called credit inquiries. This is the number of times you asked/allowed someone to review your full credit report in the last 24 months, which always happen in a credit application. There are some caveats in this number, but in general the higher this number is, the more times you have asked someone for credit. As mentioned above, multiple hard inquiries in a short period of time makes you look bad. (While CK listed this item as "low impact", a few hard inquiries would quickly add up.)

Your score already reflects the number of inquiries, but lenders could also look closely at your credit inquiries and decide that you are more risky than what the score would imply.

2. Recently opened accounts

I'm not sure if FICO/Vintage credit score models take into account this factor, but I know lenders would sometimes look at credit history to see how many accounts you have successfully opened recently and use it as another indicator of how aggressive you are in seeking credit in the recent past. Probably the most infamous example of this is Chase's 5/24 rule.

Both of these are negatives, more than offset the benefit you get from having a higher total credit limit and account numbers. So you want to avoid doing that before applying for loans. In the long run, these things don't matter as much, and pros outweigh cons.