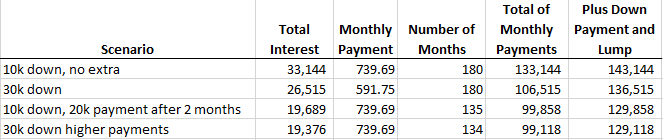

It seems you meant a $100k loan not a $100k property, it takes too long to reformat so you can get the general idea from this table.

Here's a rough amortization table, showing a monthly breakdown of year one, A/B testing a $20,000 payment in Month 4. Typically interest is charged on the average daily balance of the principle as early as you can make payments, it has a cascading effect through the remainder of the loan. The $20,000 payment saves you about $12,700 over the life of the loan and completes the loan about 4 years early, assuming it's made on month 4. If it's made in month 8 or 29 it would have a lesser effect.

Here are the forumulas if you want to build yourself an Excel (or whatever) sheet.

1st month Principle = Plug this in

Interest = principle * (0.04/12)

Payment = pmt(0.04/12, 12*15, principle)

2nd and on Principle = Prior Month Principle + Prior Month Interest + Prior Month Payment

Once you have your sheet you can play with the numbers.

Principle Int Pmt Principle Int Pmt

Month 1 -90,000 -300 666 -90,000 -300 666

Month 2 -89,634 -299 666 -89,634 -299 666

Month 3 -89,267 -298 666 -89,267 -298 666

Month 4 -88,899 -296 666 -88,899 -296 20,000

Month 5 -88,530 -295 666 -69,196 -231 666

Month 6 -88,159 -294 666 -68,760 -229 666

Month 7 -87,787 -293 666 -68,324 -228 666

Month 8 -87,414 -291 666 -67,886 -226 666

Month 9 -87,040 -290 666 -67,447 -225 666

Month 10 -86,664 -289 666 -67,006 -223 666

Month 11 -86,287 -288 666 -66,563 -222 666

Month 12 -85,909 -286 666 -66,119 -220 666

Year 1 End Balance -85,530 -65,674

Year 1 Int. & Pmt -3,519 7,989 -2,997 27,323

Year 2 End Balance -80,878 -60,213

Year 2 Int. & Pmt -3,337 7,989 -2,528 7,989

Year 3 End Balance -76,036 -54,529

Year 3 Int. & Pmt -3,147 7,989 -2,305 7,989

Year 4 End Balance -70,997 -48,614

Year 4 Int. & Pmt -2,950 7,989 -2,074 7,989

Year 5 End Balance -65,753 -42,458

Year 5 Int. & Pmt -2,744 7,989 -1,833 7,989

Year 6 End Balance -60,295 -36,051

Year 6 Int. & Pmt -2,531 7,989 -1,582 7,989

Year 7 End Balance -54,615 -29,383

Year 7 Int. & Pmt -2,308 7,989 -1,321 7,989

Year 8 End Balance -48,704 -22,444

Year 8 Int. & Pmt -2,077 7,989 -1,049 7,989

Year 9 End Balance -42,551 -15,221

Year 9 Int. & Pmt -1,836 7,989 -766 7,989

Year 10 End Balance -36,148 -7,705

Year 10 Int. & Pmt -1,585 7,989 -472 7,989

Year 11 End Balance -29,484 0

Year 11 Int. & Pmt -1,325 7,989 -166 7,871

Year 12 End Balance -22,548

Year 12 Int. & Pmt -1,053 7,989

Year 13 End Balance -15,330

Year 13 Int. & Pmt -771 7,989

Year 14 End Balance -7,818

Year 14 Int. & Pmt -476 7,989

Year 15 End Balance 0

Year 15 Int. & Pmt -170 7,989

Grand Interest& Payments -29,829 119,829 17,091 107,091