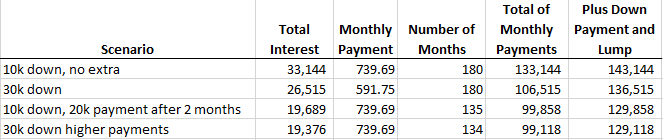

I think you've got fine answers here, but thought the following might help, I assumed you meant a $110,000 house so my numbers are based on that. The big difference in your two scenarios is that as a down-payment the extra 20k would reduce your monthly payment significantly, while as an extra principal payment it reduces the loan duration significantly. You'll notice that putting 30k down but making payments at the 10k down payment rate is pretty comparable to making a 20k extra payment after 2 months.

As noted by others, when you are putting less than 20% down you'll be faced with private mortgage insurance (PMI) that adds extra cost until you have 22% equity (based on original appraised value), not super significant here given the pre-payment plan to make the significant extra payment so early, but going for 20% down payment will save you a little money and a little hassle.