I run a small cell phone repair store and we fix many phones. Many times it's bricked phones or cracked screens. But what I want to know, do we have to charge sales tax on repair services such as these? Technically we are not selling thing anything tangible.

asked Mar 19, 2015 at 23:24

-

Replacing a cracked screen is certainly a tangible item, though the time spent installing it isn't... I don't remember how/whether NYC taxes labor– keshlamCommented Aug 6, 2015 at 13:57

Add a comment

|

3 Answers

According to the New York State Department of Taxation and Finance, your service is not exempt from taxes. Service and repair of tangible personal property are specifically itemized on this page as taxable services.

Sales of tangible personal property are subject to New York sales tax unless they are specifically exempt.

The term tangible personal property means any kind of physical personal property that has a material existence and is perceptible to the human senses (in other words, something you can see and touch).

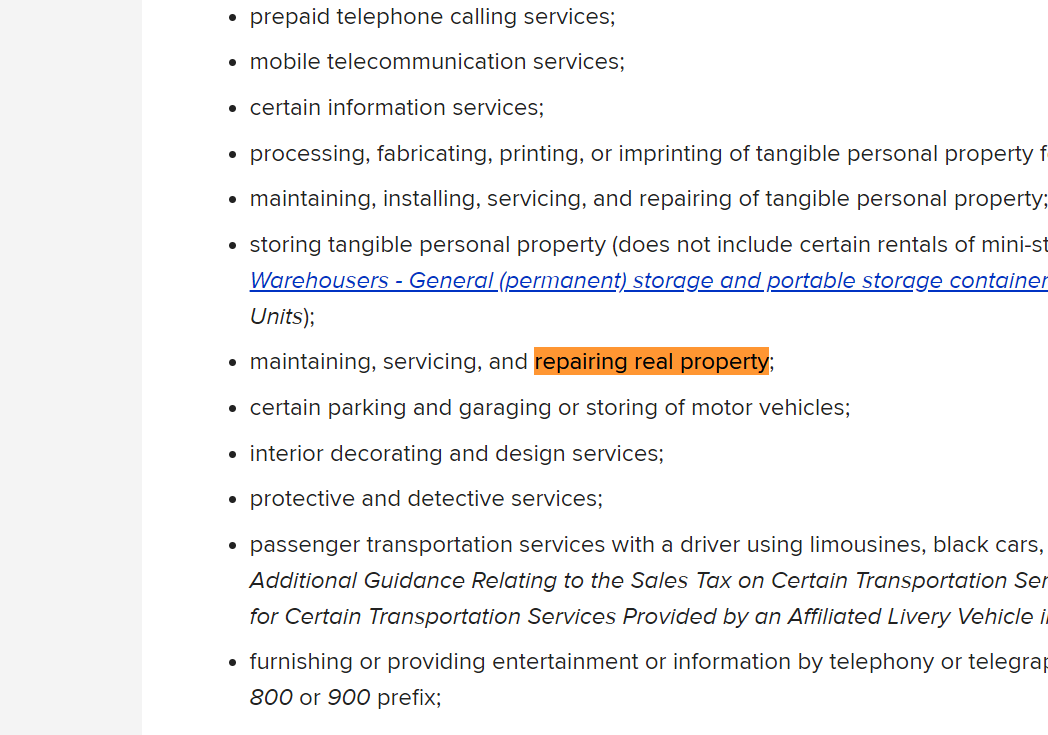

Examples of taxable tangible personal property, services, and transactions that are subject to sales tax are:

- tangible personal property:

- furniture, appliances, and light fixtures;

- certain clothing and footwear;

- machinery and equipment, parts, tools, and supplies;

- computers;

- ...

- maintaining, installing, servicing, and repairing of tangible personal property;

According to the NYC Department of Finance, the total Sales and Use tax on most tangible personal property and their associated services in New York City appears to be 8.875% in 2018:

The State and City charge sales tax on many services and on retail sales for most goods.

The total sales and use tax rate in New York City is 8.875%.

This includes:

- New York City local sales and use tax rate of 4.5%

- New York State sales and use tax rate of 4%

- Metropolitan Commuter Transportation District surcharge of 0.375%

The NYC page also lists some exempt goods and services, but mobile phone repair is not in the list of exempt services.

According to the New York State Department of Taxation and Finance, your service would appear to be exempt from taxes. However, if you are charging for tangible items, those would incur a sales tax.

-

@duckx If you bill your labor separately from the material, you only need to collect tax on the material price. The top of the website states "Sales of services are generally exempt from New York sales tax unless they are specifically taxable." Near the bottom, the taxable services are primarily limited to health and beauty type services. Commented Aug 18, 2017 at 17:43

-

3The tax ought to be on what you are charging for the parts, not what you paid for them. On the bill you provide the customer, if you do not separate the cost for the labor and parts, I suspect you may need to collect sales tax on the total bill amount. Commented Aug 18, 2017 at 19:08

The following link says servicing of any tangible property is not tax exempt:

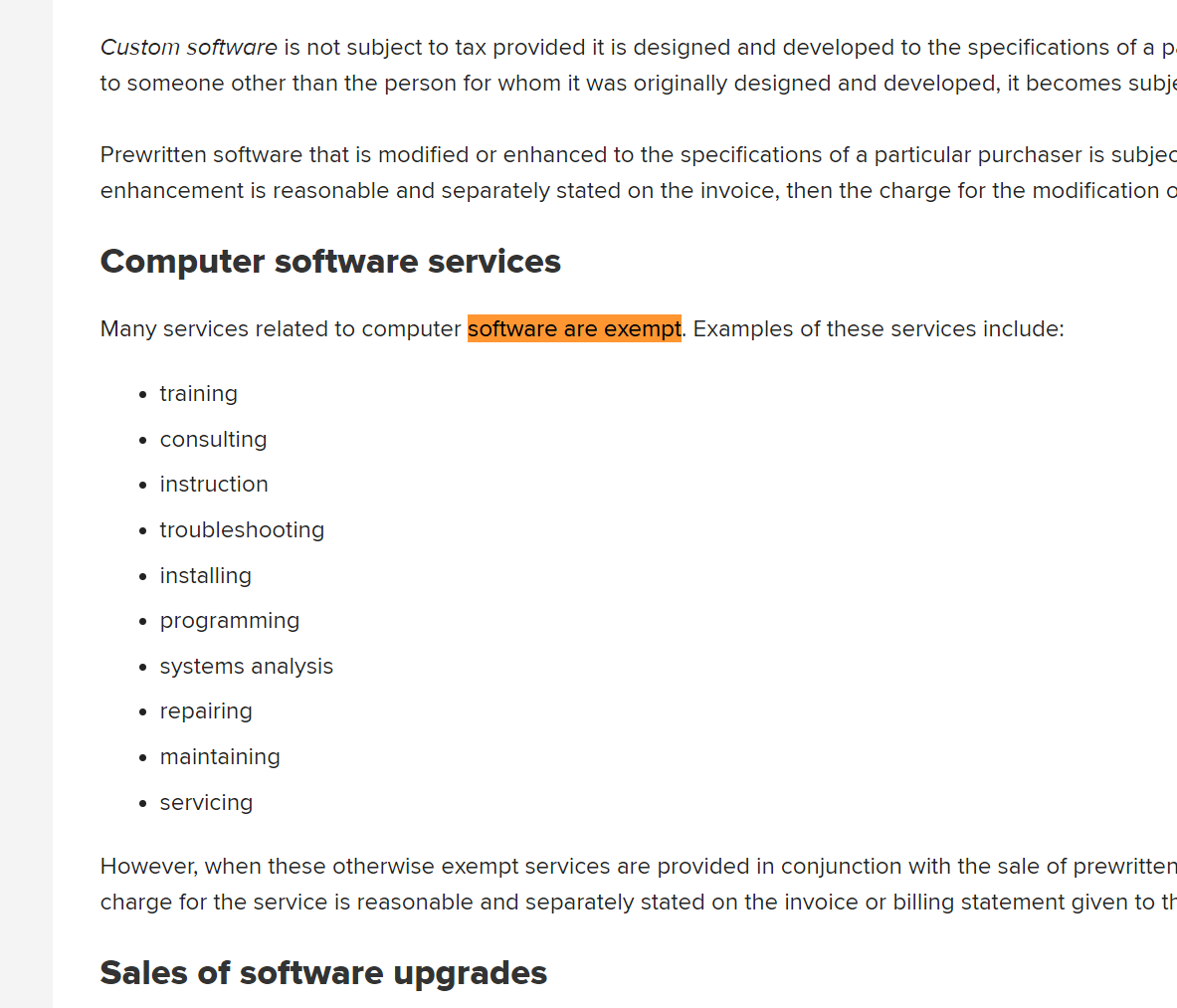

But, if the device you are "troubleshooting" or "servicing" is a software issue, it is exempt, see: https://www.tax.ny.gov/pubs_and_bulls/tg_bulletins/st/computer_software.htm

As we can see it is a contradiction in how to charge for a "software" only repair. If a customer calls you and you "troubleshoot" the software issue remotely, it is technically tax exempt according the "computer software" tax code. The question differs when the customer brings that software issue to you in person in a physical device.

answered Dec 19, 2022 at 20:34