I have several different investment accounts, and I'm trying to compare the historical performance between them.

Some of the accounts are easy: I have a couple of different accounts that are invested in one mutual fund, and I have not added any money to the account in years. I can just look at the balance of what the account was years ago, look at it today, and compare. All fees and expenses are already accounted for.

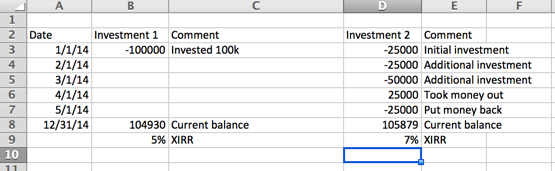

However, I have another account that is a managed account. It is continuously buying and selling various funds inside it. Of course, there are expenses, both in the managed account itself and in the funds that the account owns. In addition, I add money to it monthly. I can't just look at the balance before and after, because this wouldn't take into account the fact that I added my own money to the account each year.

Is there a good way I can compare my accounts to see which has performed the best historically?