I swing trade equity options every once in a while for fun. This morning I witnessed something I do not understand at all.

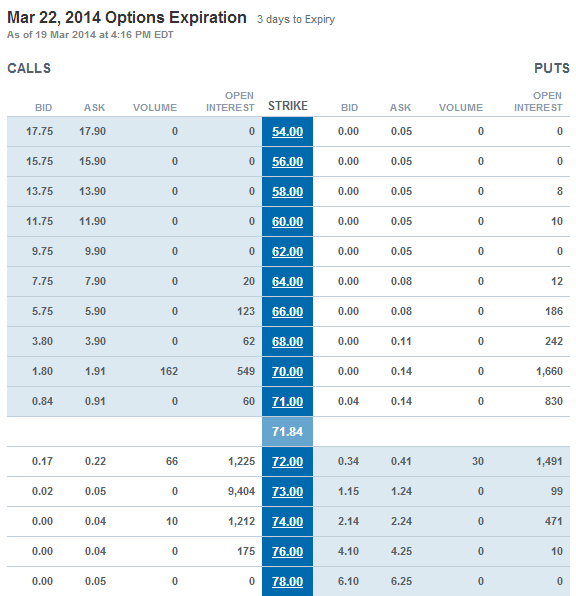

In the attached photo, why would someone purchase 6 contracts for .05 at $76. I just can't wrap my head around this!

Scenario:

- Underlying Asset:

RY.TSX - Current Price:

$71.70 - Days to expiry:

4 Days

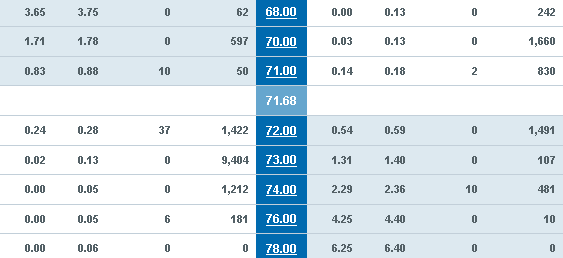

EDIT: It happened again the next day with 74, see new table with headers as per request:

My only reason for asking is because RY.TSX is the Royal Bank of Canada, this stock will not move multiple dollars in 3 days(expiry in this scenario). Why buy 10 @ 74 for .04 each instead of just buying 10 @73 for .04 which would have gone through.

If you do the math(excluding commissions):

.04 * 100(shares in a contract) * 10 contracts = $40

Stock moves to 74 and they are in the money lets say for .20

.20*100*10 = $200

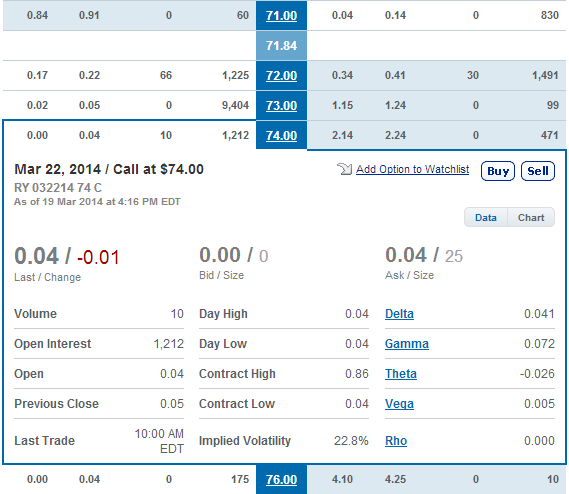

I just don't see the reward as 99% of the time you will lose this wager, it is just not worth it even if it does happen once in a blue moon. I can think of much better things to do with $40. For the skeptics another screen shot to actually confirm this order:

bear callspread, possibly a long condor or butterfly type trade. theoptionsguide.com/condor.aspx