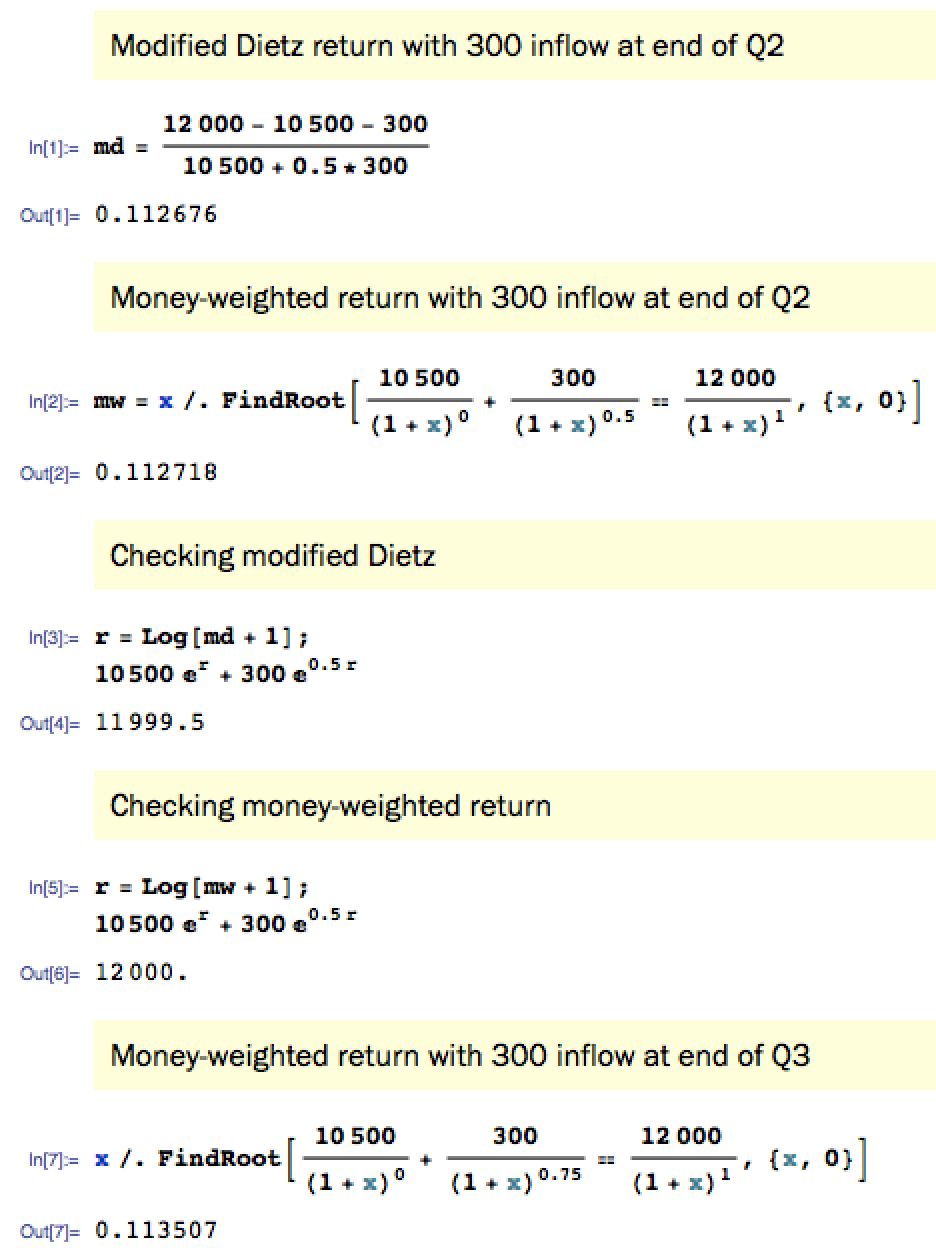

in his book "The four pillars of investing", the author describes this simple method to compute the rate of return for a portfolio that has a net inflow of cash:

Without in- or outflow, the rate of return would be the ratio of final value to initial value, minus 1.

His example: I have 12000 at the end, and started with 10500, so the rate of return is 12000 / 10500 - 1 = 14.3%.

Now if I had the same initial and final values, but due to various contributions I had also a net inflow of $300, he says that now you should subtract half of that inflow from the numerator and add half of that inflow to the denominator:

(12000 - 150) / (10500 + 150) - 1 = 11.3%

I can't really find the mathematical reason for this formula. What I personally would have done to compute a portfolio return with contributions or withdrawals is to compute the return for each period in between contributions and compound those. Say that I start with 10500 and then it grows to 11500. Then I contribute 300 dollars so I have 11800, and then it grows to 12000. The return would then be (11000 / 10500) * (12000 / 11300) - 1 = 11.4

So... is that simple method just an approximation that's good enough, or am I just using the wrong definition of total portfolio return?