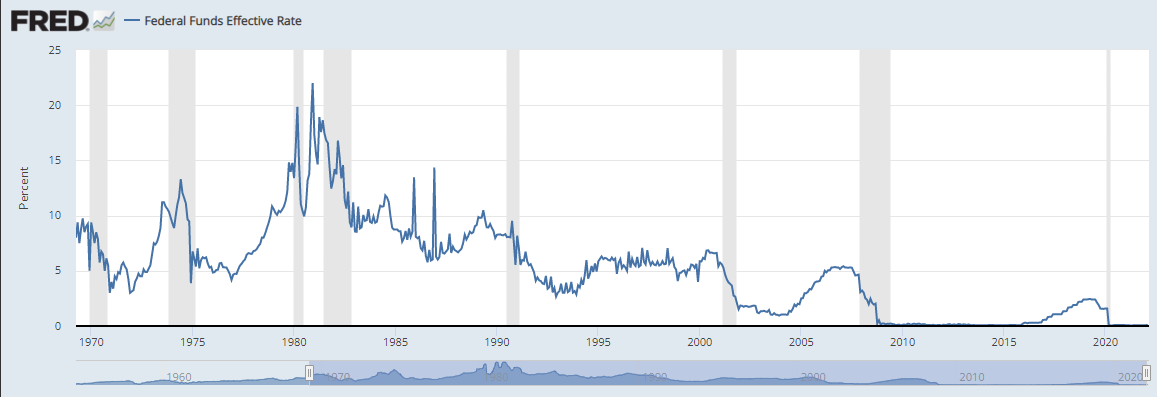

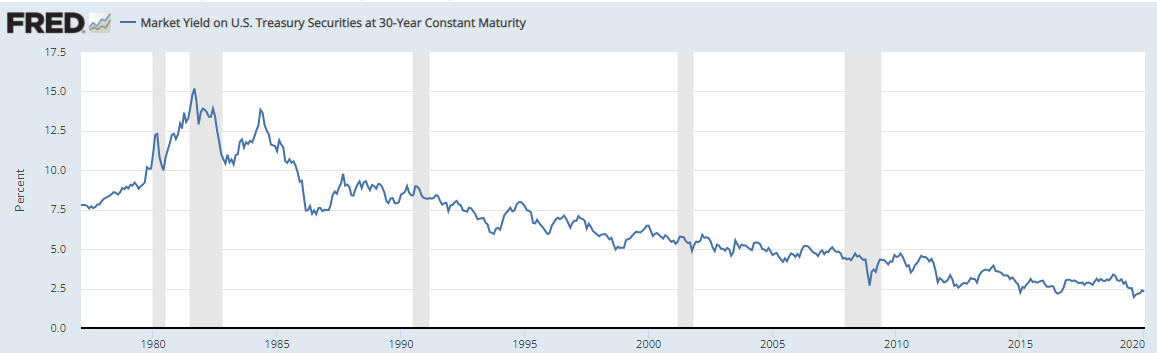

Paul Volcker raised the interest rate to over 20% in the early 80s. I was thinking to myself, if I had to manage my finances during such a time, how would I do.

According to Investopedia, bonds have an inverse relationship to rate policy. So upon a rate hike, outstanding bonds would trade at a discount to compete with new issues. I have a cursory understanding of duration and convexity (rate of change of duration) but won't pretend to understand all the mechanics.

So if I was tasked to choose a point in time (presumably) shortly before the Volcker hike to position myself, I'm not sure I have the right blueprint. Nonetheless, I'll hazard a portfolio design for $100,000:

Hypothetical 1976 plan

- Teleport myself back in time to 1976 year before the big hike

- Put everything into 1yr t-bills

- Roll over every year until 1980

- Then lock in my 15% yielding 30yr (with the clairvoyance that there are no further hikes)

- Then in 2012 or so, I will have had a decent return

But I'm not that confident I played it right, feels like I'm missing something. Inflation-adjusted returns might be bad. Maybe TIPs would have been better?