I keep encountering examples of large option trades on stocks whose IVs are extremely low since their price is pegged by a pending buyout. Today's example is WUBA, an ADR for a Chinese classifieds web site like Craigslist. It has an agreed buyout offer from June at $56 per share.

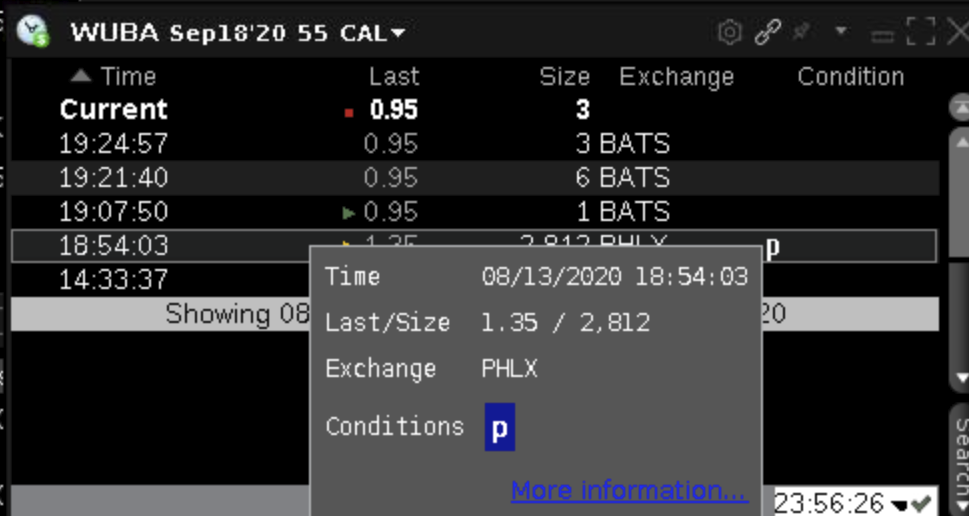

Despite that, it is possible to observe the purchase today of a large block of September $55 calls:

(Trade for 2,812 WUBA Sep 18 55c @ $1.35, total value: $379,620)

The 'P' condition code indicates this was part of a two-legged order involving stock, and indeed it is possible to observe the corresponding stock order:

(Trade for 281,200 WUBA @ $55.78, total value: $15,685,336)

The '7' condition code in the stock sale indicates this is part of a "qualified contingent trade", the definition of which is not easily summarized (see page 143 here), but at least confirms this is part of a multi-legged order.

I could not determine whether the stock was bought or sold, however it is at least possible to see it likely was not sold short, as the FINRA Reg SHO CSV reveals only 59,217 shares were sold short today (6.4% of all volume, total short float is currently 1.28%).

Another detail is that WUBA have an earnings report due on 19th August, but again I'm not sure how earnings relates to an agreed buyout. Could excess earnings lead to a revised or abandoned offer?

Due to the size and nature of the order, I considered that possibly a fund was repositioning itself somehow, and checked ETF DB for any matching fund. The top two funds listed there, DINT and DWLD, have WUBA holdings around the $11m mark, which seems insufficient to describe the order.

Supposition

As the call option's open interest fully reflects the size of the trade, it seems new contracts were written to satisfy this trade. (I do not understand the option creation/destruction process, but have certainly observed OI reported much lower than daily volume, presumably an artefact of that process)

Since short volume was insufficient to describe the order, the only possibilities are that the participant purchased the shares at the same time as purchasing the calls, or that they already owned the shares, and sold them at the time of purchasing the calls.

Since both stock and option orders are flagged as part of some multi-legged institutional order, it seems the orders are definitely related and that for example the stock order was not due some delta-neutral hedging strategy of a market maker selling the calls.

Of the possibilities above, it seems to me most likely that the trader was selling the shares, and possibly hedging the sale with a much smaller options position (the cost of the options are 2.4% of the overall stock sale price in this case).

But hedging against what? Could a strong earnings report cause the stock price to increase despite the buyout offer?

I'm not really sure if this is a question about options strategies or buyouts. How would you interpret this trade?