I am looking at historical data for the iShares S&P 500 GBP Hedged UCITS ETF (Acc) Exchange Traded Fund (ETF), with Epic ID IGUS. The objective of the ETF is to track the performance of the S&P500 hedged back to GBP, in order to insulate against any PnL originating from moves in the GBPUSD FX rate (technically it seems to be tracking a GBP-version of the S&P500 but this should have no influence in practice I think):

The Fund seeks to track the performance of an index composed of 500 large cap U.S. companies which also hedges USD currency in the index back to GBP on a monthly basis.

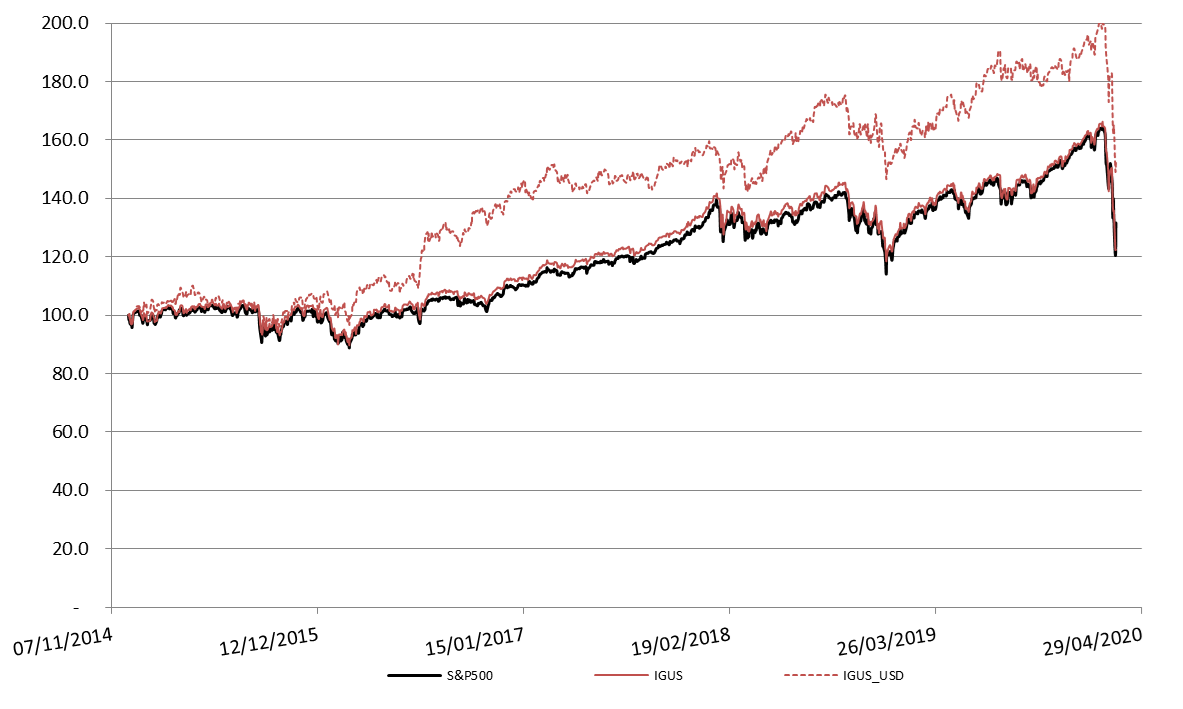

Now, according to the webpage itself, IGUS is an accumulating ETF so that dividends are reinvested automatically. As far as I know this is not the case for the S&P500 index, which is calculated on a total return basis but assuming distribution of dividends, hence no compounding. Therefore, over long periods, I would expect the quotation of IGUS to gradually diverge upwardly with respect to the S&P index. However, when looking at historical data from investing.com for a) the S&P500 index, and b) the IGUS ETF, I actually find that IGUS tracks the S&P500 very closely (I have also added the evolution of IGUS with daily conversion to USD):

I would expect IGUS (red continuous line) to gradually diverge from the S&P500. Why is that not the case? It does not look to me like IGUS is reinvesting dividends, there is no compounding here. On the other hand, other S&P500 accumulating ETFs do show compounding effects even after expressed in GBP terms, such as CSP1. Can anybody explain this?