How can I best calculate the fiscal impact of these two choices?

- Take a $50k distribution from a traditional IRA to offset an expense, thus saving taxes now.

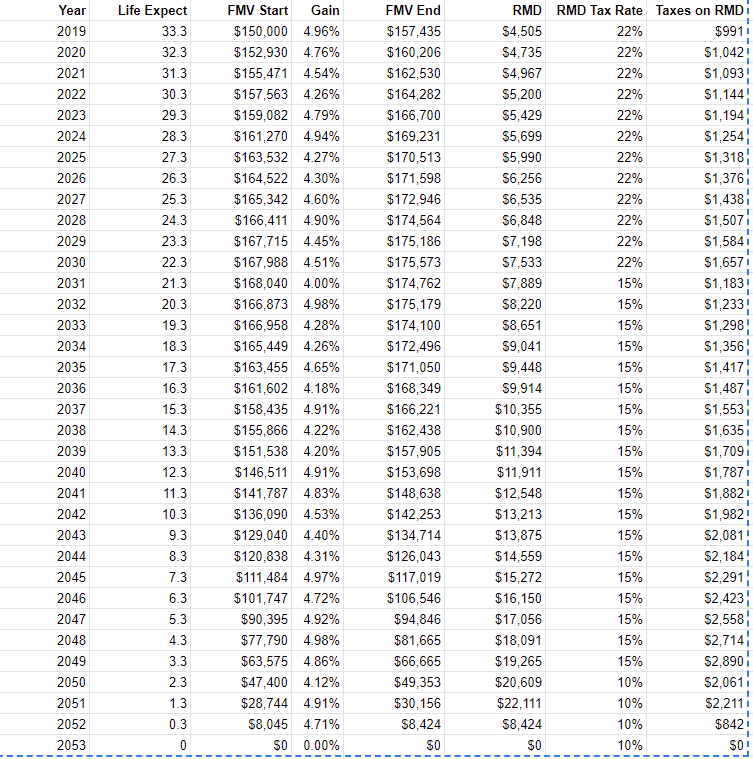

- Leave the money in the IRA, allowing tax deferred growth to continue over 33.3 years.

The $50k deduction will be lost if not offset by income. The current tax savings would be 24% of half of it, or $6000.

If left in the IRA, the distribution schedule is over 33.3 years, with the same split (one beneficiary currently pays 22/24% tax, the other is indigent and does not pay tax). Meaning the first year there would be $50,000 more in the IRA, the second year $50,000 minus the $1500 RMD, and so on. So the first year the $50,000 might earn 6% or $3000 which would then be dribbled out over time as RMD and taxed. Over time the tax paying beneficiary might retire and drift down in tax bracket.

How can I best calculate the impact of each choice? Yes I can set up a spreadsheet, but there are so many assumptions....