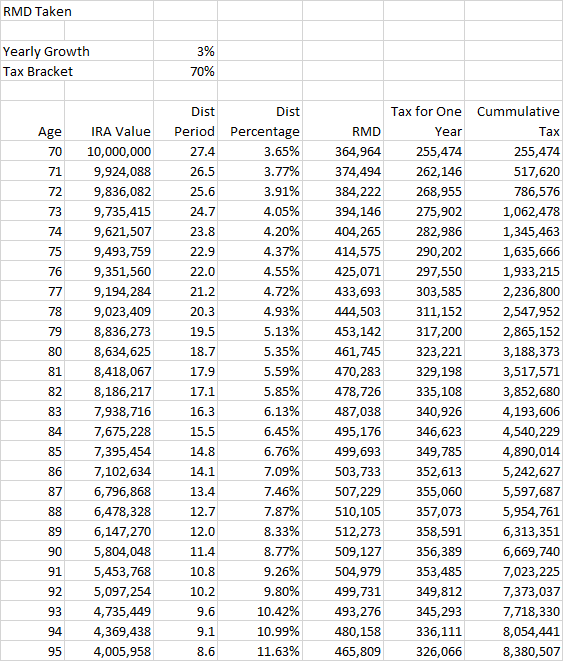

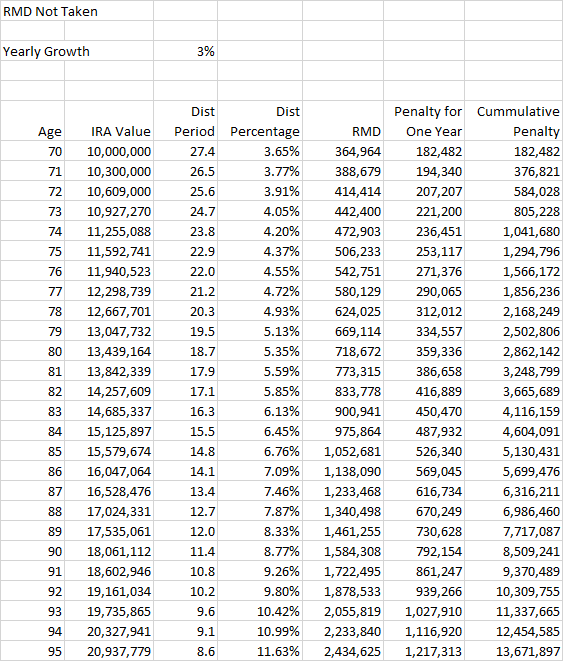

Could it ever be advantageous for a wealthy retired person over the age of 70-1/2 with significant taxable investment income to intentionally fail to take a Required Minimum Distribution (RMD) from an IRA and just pay the 50% penalty that is imposed for failure to take the RMD? The penalty could be paid from non-IRA funds, thereby allowing the IRA funds to continue to grow tax-free.

For example, if income taxes for the wealthy were to increase due to changing political ideologies, a 50% penalty in lieu of taxes might be a bargain. Currently (2019) the top federal income tax rate is 37%. The top California state income tax rate currently adds another 12.3% for a top marginal tax rate of 49.3% for taxable income in the $500K range. A Quora post says that the IRS reported 898,415 tax returns with an AGI over $500K in 2011, so some taxpayers are probably in this situation already.

Even a wealthy resident of a state with moderate income taxes could benefit from paying the penalty if maximum federal tax rates ever return to historical levels. The top federal tax rate was 70% as recently as 1980, and it was an unbelievable 94% during WWII. Historical tax rates here.

So am I missing something or could this be a viable strategy when a wealthy person doesn’t need the income from their IRA and would rather let it grow tax-free until the end of their life, to be left to individual beneficiaries in lower tax brackets?