In this case, the mortgage constant (or loan constant or debt constant) is the (in my case, annual) ratio of constant payments to the original amount, like here: http://www.double-entry-bookkeeping.com/periodic-payment/how-to-calculate-a-debt-constant/

Suppose we have an annual interest rate of 4.565% and 360 payments (30 year loan). In Excel, we can specify the following formula:

PMT(0.04565/12, 360, -1, 0, 1) * 12

Where present value is $1, future value is $0, and Type=1 signifies that payments are due at the beginning of the period. The result is 6.1034%.

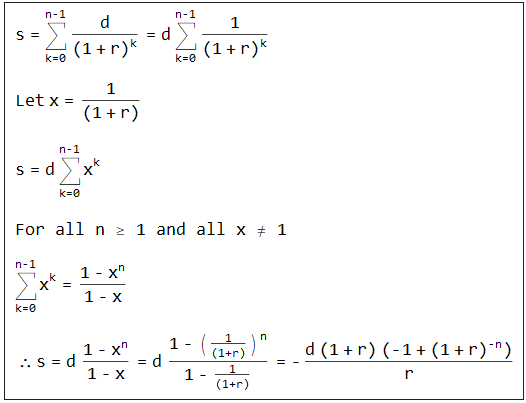

When I apply the mathematical formula, it assumes that payments are made at the end of the period (or am I wrong?), so where

Debt Constant = (Interest Rate/12) / (1 - (1 / (1 + Interest Rate/12))^n) * 12

= (0.04565/12) / (1 - (1 / (1 + 0.04565/12))^360) * 12

= 6.1267%

How is the formula adjusted to account for the payments made in the beginning of the period, since the actual value for the purposes of this calculation is not known? Or am I misunderstanding something?

Thanks in advance.