Extending the example in the link.

d is the periodic payment

p is the loan amount

r1 is the periodic rate for the first m periods

r2 is the periodic rate for the next n periods

r3 is the periodic rate for the next o periods

p = 100000

r1 = 0.03

m = 2

r2 = 0.04

n = 3

r3 = 0.05

o = 2

Discounting each payment to net present value:

pv1 = d/(1 + r1)

pv2 = d/((1 + r1) (1 + r1))

pv3 = d/((1 + r1) (1 + r1) (1 + r2))

pv4 = d/((1 + r1) (1 + r1) (1 + r2) (1 + r2))

pv5 = d/((1 + r1) (1 + r1) (1 + r2) (1 + r2) (1 + r2))

pv6 = d/((1 + r1) (1 + r1) (1 + r2) (1 + r2) (1 + r2) (1 + r3))

pv7 = d/((1 + r1) (1 + r1) (1 + r2) (1 + r2) (1 + r2) (1 + r3) (1 + r3))

p = pv1 + pv2 + pv3 + pv4 + pv5 + pv6 + pv7

6.08738 d

So p = 6.08738 d therefore d = 100000/6.08738 = 16427.43

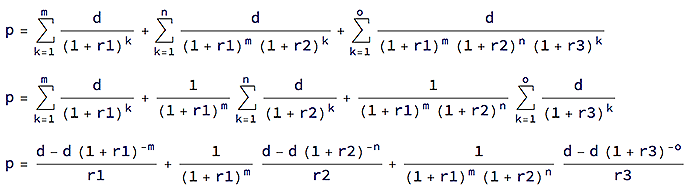

Expressing the above using summations and formulae:

p = (d - d (1 + r1)^-m)/r1 +

1/(1 + r1)^m (d - d (1 + r2)^-n)/r2 +

1/((1 + r1)^m (1 + r2)^n) (d - d (1 + r3)^-o)/r3

6.08738 d

There is a clear pattern to extend the formula for any number of changes. Here is the mathematical formula, but it does not simplify:

With

z[1] = r1, z[2] = r2, z[3] = r3, etc.

v[1] = m, v[2] = n, v[3] = o, etc.

f[3]

6.08738 d

∴ d = 100000/6.08738 = 16427.43

Returning to the three-rate formula and rearranging for d:

p = (d - d (1 + r1)^-m)/r1 +

1/(1 + r1)^m (d - d (1 + r2)^-n)/r2 +

1/((1 + r1)^m (1 + r2)^n) (d - d (1 + r3)^-o)/r3

∴ d = (p r1 (1 + r1)^m r2 (1 + r2)^n r3 (1 + r3)^o)/

(-r1 r2 + (1 + r3)^o (r1 (r2 - r3) +

(1 + r2)^n (r1 + (-1 + (1 + r1)^m) r2) r3))

= 16427.43