Investment advice is often written from the perspective of a large domestic economy, where global effects have less impact. I live in Australia, where GDP is $1.13 trillion and our stock exchange has a market capitalisation of $1.6 trillion — around 1/20th of the United States'. Suppose I want to allocate 60% of my assets to stocks, 30% to bonds, and 10% to cash. How should I divide the allocations between Australian and foreign assets?

Most Australian superannuation funds are weighted in favour of Australian shares. For example, AustralianSuper's default portfolio currently allocates 23% to Australian shares and 35% to international shares. Individual investors are also less likely to purchase foreign stocks because of higher transaction costs and unwanted currency risk.

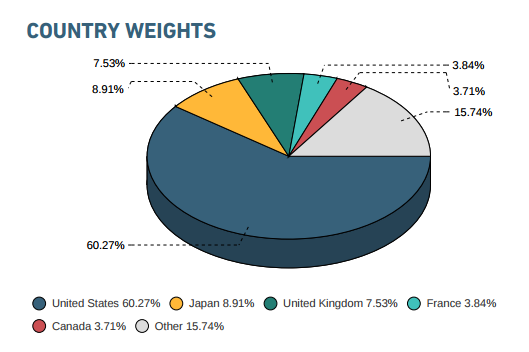

However, mutual funds denominated in Australian dollars such as the Vanguard International Shares Index Fund are available. This fund tracks the MSCI World (ex Australia) index:

Since Australia is taken out of the index, I still don't know how to decide on the weighting to give to Australian assets in my own portfolio. Currency risk and higher transaction fees are good reasons for a strong bias in favour of domestic assets. I'm not a forex trader, so it's probably pointless for me to hold any foreign bonds or cash.

Conversely, if I want to allocate 60% of my portfolio to diversified stock holdings, why should I have any bias in favour of my local economy? Should the composition of my stock portfolio track the global economy, like the MSCI World index?