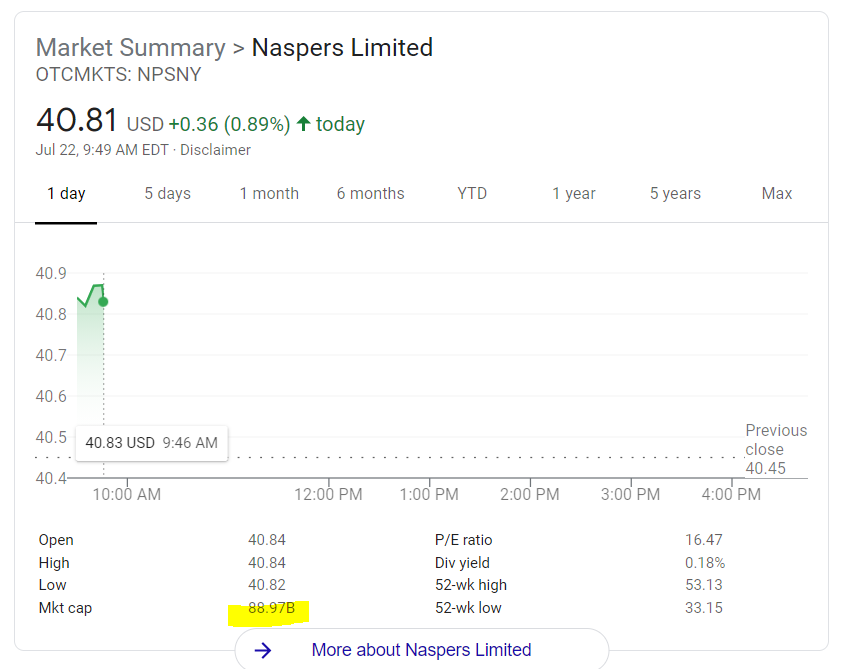

The market capitalization of Naspers is approximately 1.3 trillion ZAR, which is equivalent to approximately 75 billion EUR.

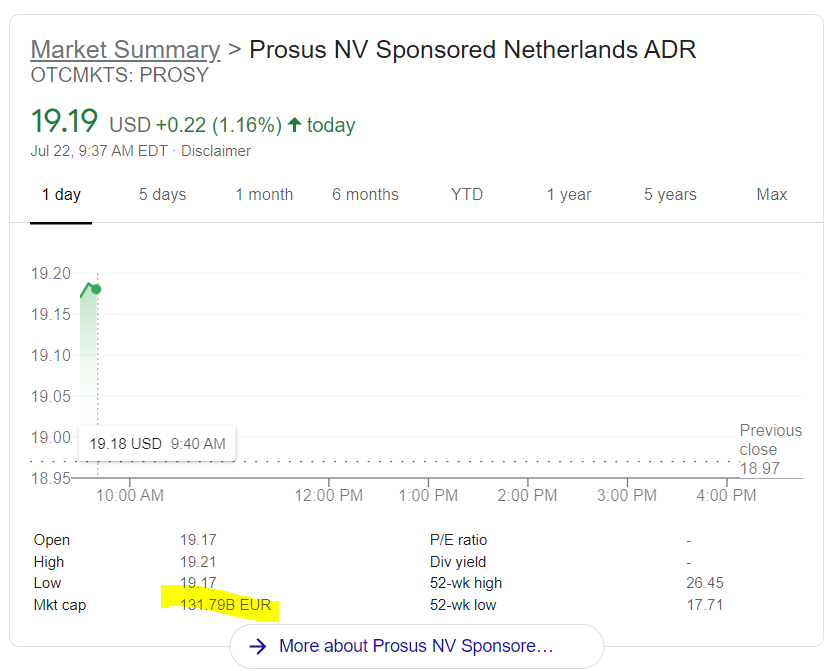

The market capitalization of Prosus is approximately 130 billion EUR.

If not mistaken, Naspers owns about 70% of Prosus, so Naspers' stake in Prosus is worth about 90 billion EUR. Naspers' stake in Prosus is worth more than Naspers' market capitalization. There is a discrepancy of 15 billion EUR.

This discrepancy is called a "negative stub value". A historical US example of this is the spin-off of Palm, Inc. from 3Com Corporation in 2000, which also had a negative stub value in the billions of dollars.

The creation of Prosus itself was motivated by Naspers' negative stub value from Naspers' stake in Tencent. It appears that the creation of Prosus has not really solved their negative stub value problem so far.

So yes, it is possible for a parent company's stake in a subsidiary to be worth more than the market capitalization of the parent company. The situation could be persistent if it is difficult for market participants to conduct arbitrage to remove the discrepancy.

Further reading: Limited Arbitrage in Equity Markets by Mark Mitchell, Todd Pulvino and Erik Stafford examines the difficulties in arbitraging 82 negative stub value situations between 1985 and 2000.