I'm trying to find a way to calculate the price of a home I can afford based on my potential downpayment, the monthly rent I can afford, and the interest of a potential loan. I've seen questions like this and this and I've consulted other sites like this, but I can't seem to find one with the home value as the output.

The structure I need is an equation that spits out a total home value (e.g. $800,000) with the following variables:

- Monthly Mortgage Payment

- Term of Loan

- Interest Rate

- Downpayment

I'm fine assuming it's a standard mortgage, but if there was a way I could try out different types (ARM, etc.) that would be a plus.

One issue: I know Excel has the PMT function, but I want to know what's happening, so I need it to be in basic, PEMDAS-able operations.

Can anyone lead me in the right direction?

Additional Information:

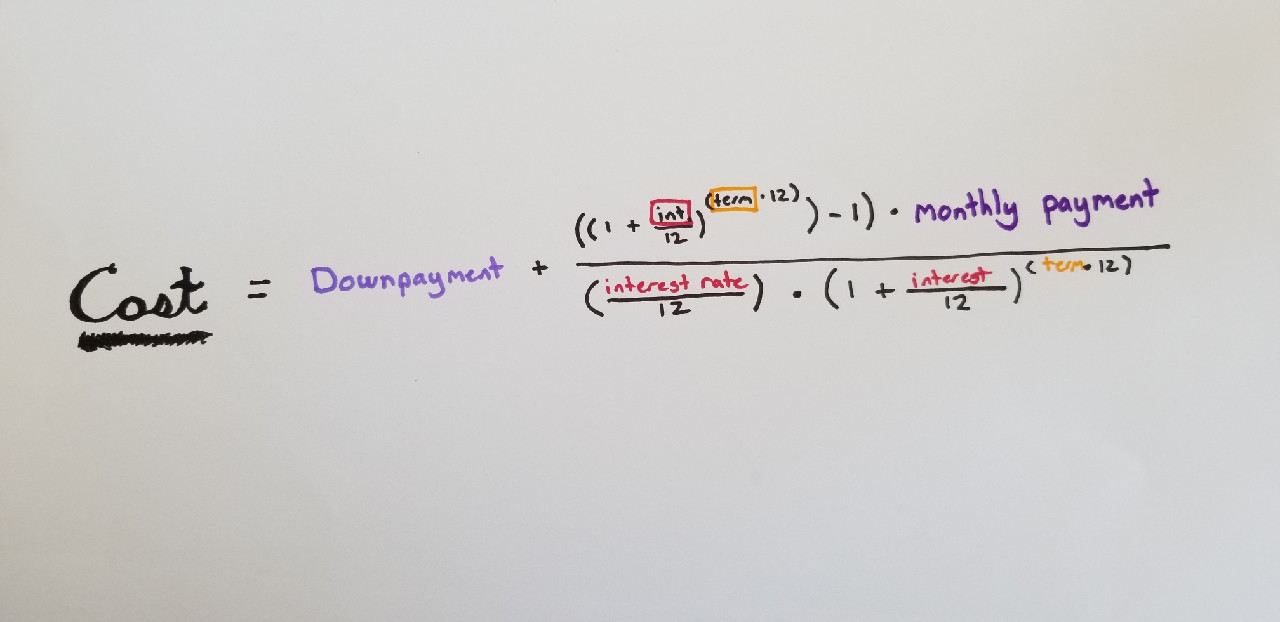

Here's a picture of my (unfortunately-handwritten) attempt: