An index fund buys all bonds in some index based on their relative weights (how much the bond appears in the index or what percentage of the market the bond is).

A managed fund does research and buys bonds that it expects to do better than other bonds. Doing the research costs money, so they charge higher fees. In theory the research is supposed to make the bonds they choose do better than the index as a whole. In practice, indexes often perform at least as well as managed funds after the fees are deducted. Some managed funds outperform their indexes for some period of time. It's unclear if they are superior investors or just lucky.

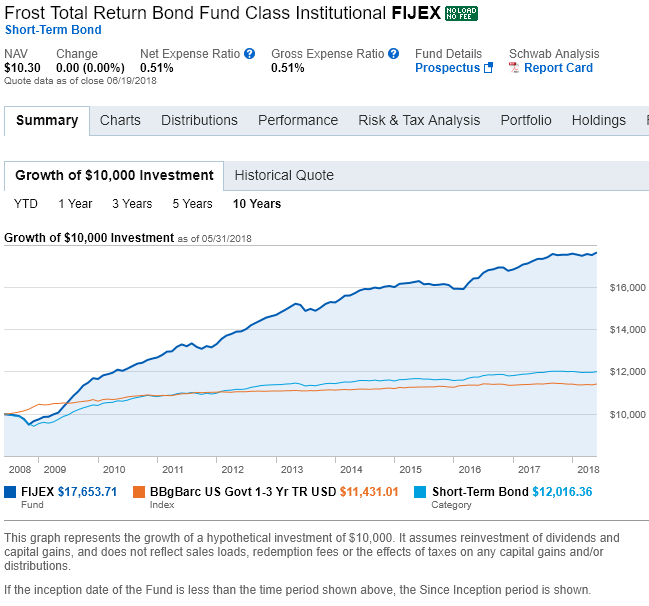

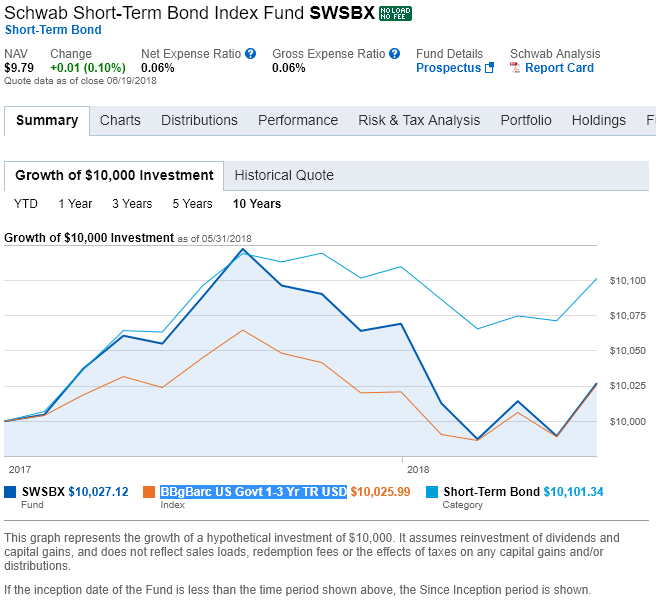

Even if the index fund is new, you should be able to estimate its performance by looking at the reference index. In your images, the reference index for both funds is BBgBarc US govt 1-3 Yr Tr USD. As you might guess, the index fund's performance is very similar to that of the index. The managed fund's performance is showing higher. You should expect the index fund to continue to track the index closely. The past good performance of the managed fund is not evidence that it will outperform in the future, but it might.

As a caveat, note that the managed fund has sometimes underperformed the index for some time periods. I can see that just looking at the ten-year performance in your image. This is normal and expected. Be careful about leaving the fund based on short term performance. You might be leaving just as the fund is about to pick up.

For example, the index fund might (or might not) outperform the managed fund in the coming year. That could indicate that the managed fund knows something that the index fund does not and is due for a period of strong growth. Or it could indicate that their luck has run out.

As they say, past performance does not guarantee future results.