I see you've marked an answer as accepted but I MUST tell you that STOPPING your 401k contribution all together is a bad idea.

Your company match is 100% rate of return(or 50% depending on structure). I don't care what market you look at, or how bad a loan you take out, you will not receive 100% rate of return, or be charged 100% interest.

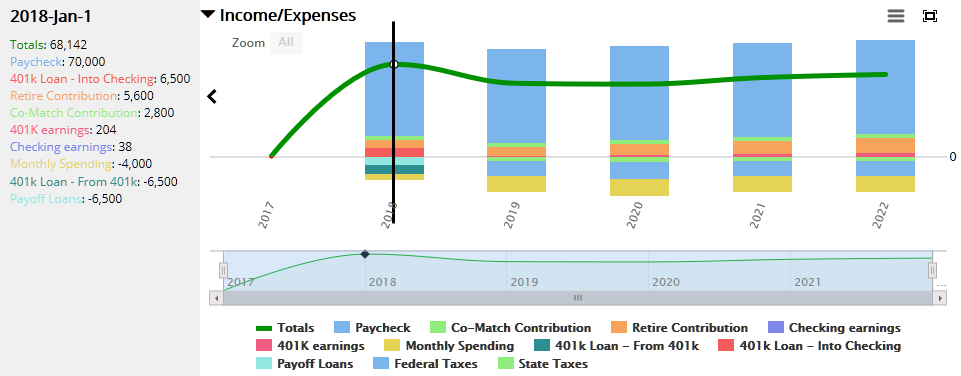

Further, taking out a loan against your 401k effectively does two things:

It is a loan that must be repaid according to the terms of your 401k

AND in every 401k I've ever encountered, you cannot make contributions to the 401k until the loan is repaid.

This in effect stops your contributions, and will almost certainly save you very little on your interest rates on your current loans.

I have 4 potential solutions that may help achieve your goal without sacrificing your 401k match and transferring the debt from one lender to another, but they are conditional.

Is your company match 100% up to 4% of your salary, or 50% of your contribution (up to a limit you have not yet reached)?

This is important. If it is 100% up to 4%, stop committing the additional 4% and use that to pay down your debt...and after ward set up that 4% as auto pay into an IRA, not into the 401k. An IRA will make you more money because YOU have control over its management, not your employer.

If it is 50% match, contribute until the match is met because you cannot get 50% rate of return anywhere, then take your additional monies and get an IRA. As far as your debt, in this scenario simply suck it up and pay it as is. You will lose far more than you gain by stopping your contributions.

If you simply must reduce your expenses by 150$ month try refinancing the mortgage and rolling the 6500$ into it. If you get a big enough drop in the interest rate you could still end up paying less.

OR

If you cannot make the gain there, try snowballing the three payments. You do this by calling your student loan vendor and telling them you need to make much smaller payments, like even zero depending on the type of loan. Then take ALL of the money you are currently spending on the 3 loans and put into the car payment. When it's gone, roll the whole thing into the higher interest student loan, then finally roll it all into the last student loan. You'll pay it off faster, and student loans have lots of laws and regulations regarding working with payers to keep them paying something without breaking them.

WHATEVER YOU DO, DO NOT STOP YOUR CONTRIBUTIONS. 50% OR 100%, THAT MONEY IS GUARANTEED AT A HIGHER RATE OF RETURN THAN YOU CAN GET ANYWHERE, ESPECIALLY GUARANTEED.