This question relates to a Dependent Care Flexible Spending Account (FSA) account in the USA. I'm aware that contributions to an FSA are not available to self employed persons, and not deductible if one spouse is 'stay at home'.

What rules apply to a working spouse with an employer FSA, plus a self-employed spouse? And if money is put aside in an FSA, but the final taxable income of either spouse is too low, are there penalties or forfeit funds? Self employed persons may run a profit or loss in a given year, even if working full time.

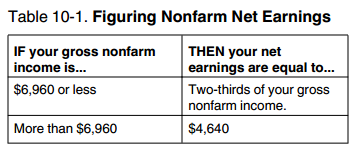

Reference documents include http://www.irs.gov/publications/p969/ar02.html and http://www.irs.gov/publications/p502/