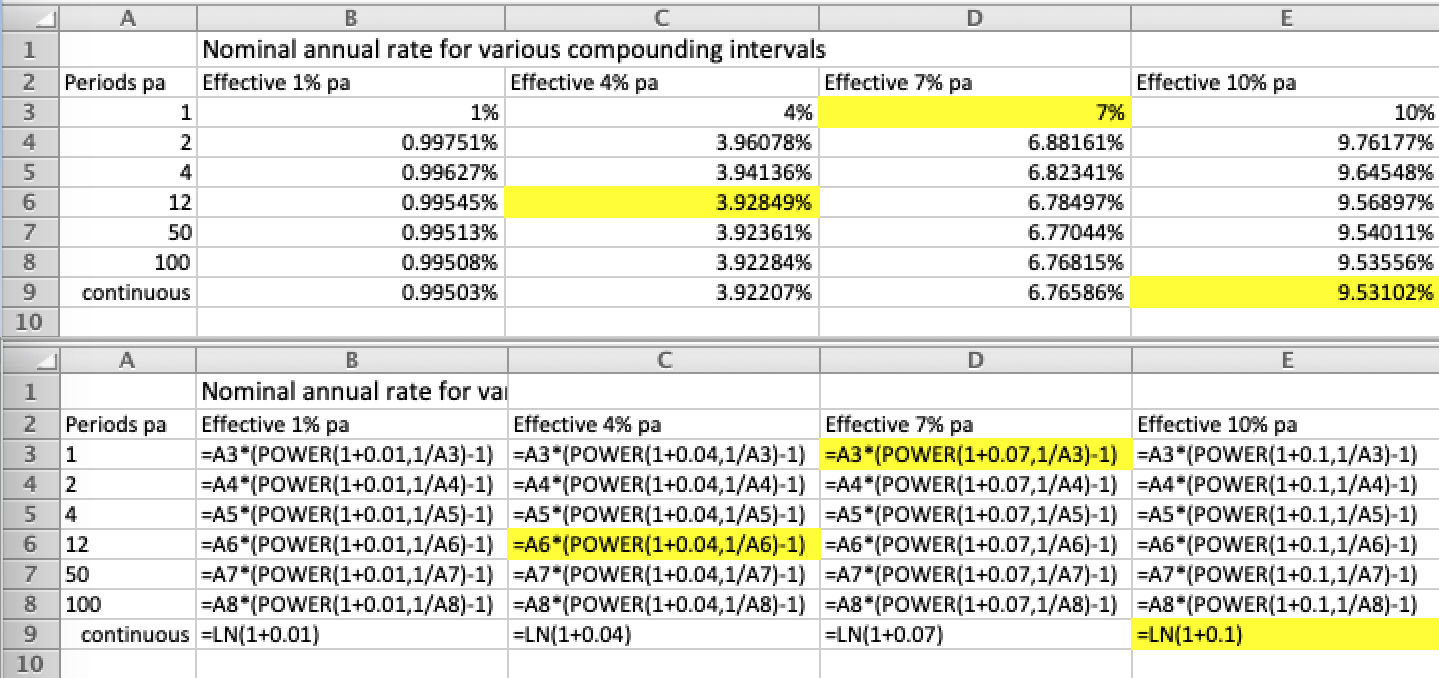

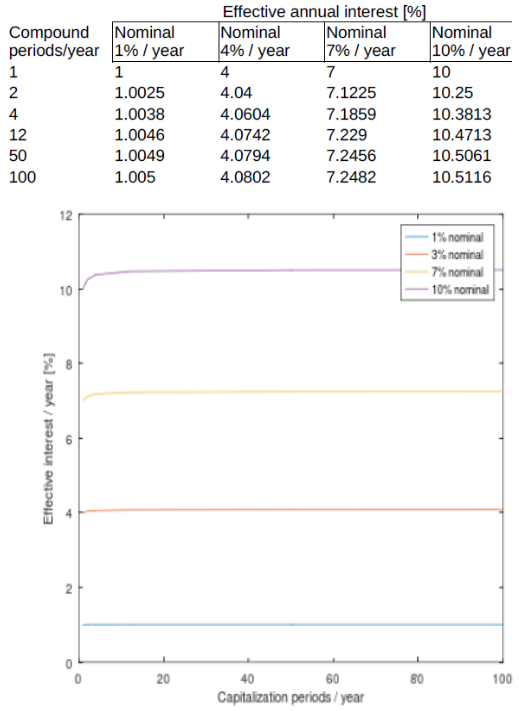

I tried to get a sense of how much difference is makes when a nominal annual interest rate is capitalized multiple times per year, especially as the number of capitalizations approaches infinity, i.e., continuous compounding. I calculated effective annual interest rates for nominal rates of 1%, 3%, 7%, and 10%. The number of capitalizations / year were 1, 2, 4, 12, 50, and 100. 100 is when the curve flattens out, so it's a good proxy for continuous compounding (infinite capitalizations / year).

It seems that multiple capitalizations / year only starts to make a significant difference for nominal interest rates of 5+ % / year. Does this look reasonable?

Matlab/Octave code

cCapPrYr = [ 1 2 4 12 50 100 ]'; % Column of capitalization periods/year

rNomInt100 = 1:3:10; % Row of nominal interest [%]

EffInt100 = zeros( length( cCapPrYr ), 0 );

for NomInt = rNomInt100 / 100

EffInt100 = [ EffInt100 100*( ...

( 1 + NomInt ./ cCapPrYr ) .^ cCapPrYr - 1

) ];

end % for NomInt100

plot( cCapPrYr, EffInt100 )

xlabel('Capitalization periods / year')

ylabel('Effective interest / year [%]')

legend('1% nominal','3% nominal','7% nominal','10% nominal')

EffInt100

% 1.0000 4.0000 7.0000 10.0000

% 1.0025 4.0400 7.1225 10.2500

% 1.0038 4.0604 7.1859 10.3813

% 1.0046 4.0742 7.2290 10.4713

% 1.0049 4.0794 7.2456 10.5061

% 1.0050 4.0802 7.2482 10.5116.

%

% Imported into LibreOffice Calc, printed PDF must be cropped:

% pdfjam --keepinfo --trim "2.5in 8.3in 1.5in 1in" --fitpaper true \

% EffIntVsCapsPrYr.pdf --outfile EffIntVsCapsPrYr-jam.pdf