I paid it off. (Before you congratulate me, I'd like to remind you that I imagine this must be how it feels getting released from prison.)

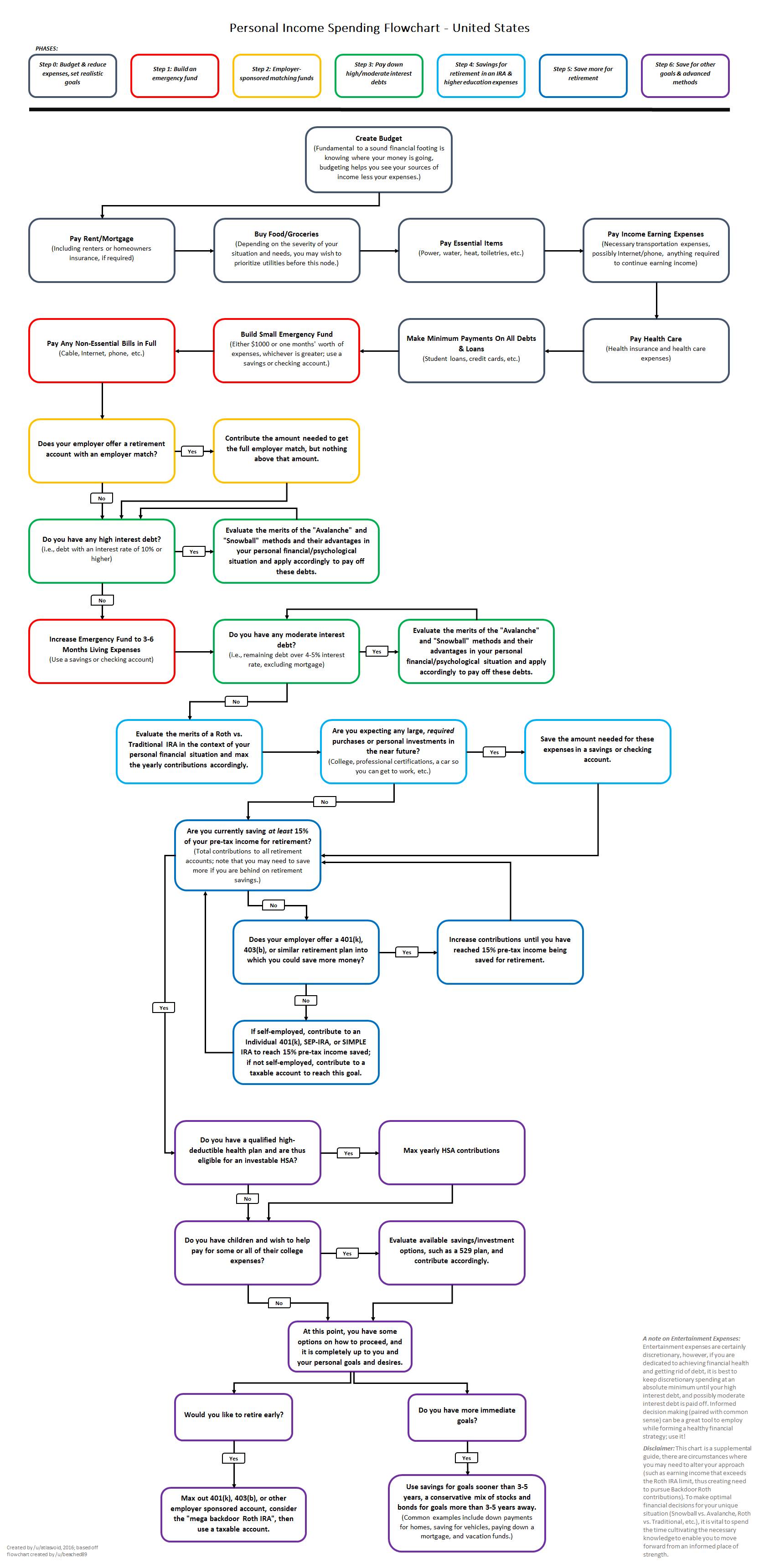

But now there's $1100/month that I was paying toward that monster, that now will be going to other things. I read an article recently (by chance), where the advice giver said to split your income in three pieces: 20% for retirement savings, 50% for living expenses, and 30% for fun...

So the question is whether those are good figures. A related question is that I have some serious home improvement to do, which kinda messes with that plan.

I plan on seeing a financial planner in the new year, but I'd like your thoughts on how to prepare for that, and my other questions...