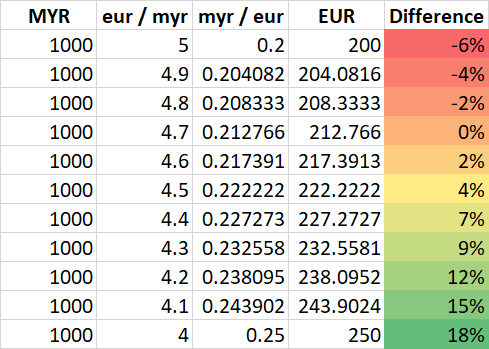

Assuming that you must eventually convert this money to EUR, follow the Law of Large Numbers. Pick a time period you can live with, and do multiple transfers over that period. Each transfer should be the of same amount, and with the same number of days between transfers.

If today's exchange rate is unlucky, and it goes up later, you won't miss out completely on the better exchange rate. OTOH, if today's exchange rate is much better than what the future holds, then at least you got some of your money out at a better rate. In other words, you're hedging against the fact that your predictions could be wrong, and you're ensuring that your percent of loss/gain are (on average) the same as anyone else doing a MYR -> EUR conversion at any time during the time period in question.

To compensate for any fixed fees involved, you'll want to use large enough chunks of money so that the fee as a percentage of the amount being transferred at once is minimized; Perhaps you'll want to maintain a EUR savings account so that you can transfer the money from EUR to stocks in different sized chunks, and at a different frequency.

How I found the answer

Let's reframe the question until it's answerable.

Scenario 1

Let's assume that the exchange rate you desire does win out in the end, but it takes 12 months. You also have to consider the opportunity cost of having not invested in the stocks you desire during those 12 months.

So, another question you should ask is, "Will the European stocks recover faster than the exchange rate?" As long as they recover at the same rate, it doesn't matter when you invest; the outcome is the same. Again, that's assuming that the exchange rate does "recover" to your personal expectations.

Or, what if the exchange rate doesn't recover, and the stocks decline as well?

Then the question becomes, "Which one will decline more slowly?"

Scenario 2

Let's consider another scenario. Imagine a man named Bob, who gets paid in EUR but whose living expenses are paid in MYR. He keeps a savings account in EUR, and each month, Bob transfers a certain amount, smaller than his income, from his savings into MYR for his expenses.

Bob is essentially betting that the European economy will outperform the Malaysian economy in the future; or that its risk of volatility is lower. If he believed the reverse, he would transfer all of his income to MYR, and maintain a MYR savings account.

That is the scenario without stocks involved.1 You need a certain amount of currency in MYR to support your daily life; but everything else should be stored in the currency you expect to do better. According to the trend of the exchange rate to this current moment, you would have been better off to maintain the bulk of your savings in EUR, even if you didn't invest it. That doesn't tell you where the trend is headed, though. In a month or year, the exchange rate might tell the opposite story.

1 The primary difference between you and Bob is that the inconvenience of transferring currency happens at a different times. Bob is forced to make this decision with every paycheck; you are forced to make it every time you re-balance your savings and stock holdings.

The frequency of transactions also changes up the risks over time: Bob's personal outcome will more closely match the overall state of affairs than yours. You could get very lucky (or unlucky). Bob cannot get very lucky or unlucky, because he made small currency transfers at consistent times.

So, if you plan to convert to EUR anyway, perhaps you should divide the transactions across the amount of time you are okay with waiting, so that you don't get caught off guard