I don't think this duplicates Why do banks give small APR loans, because I'm asking HK, and APR = 3% here not $4%.

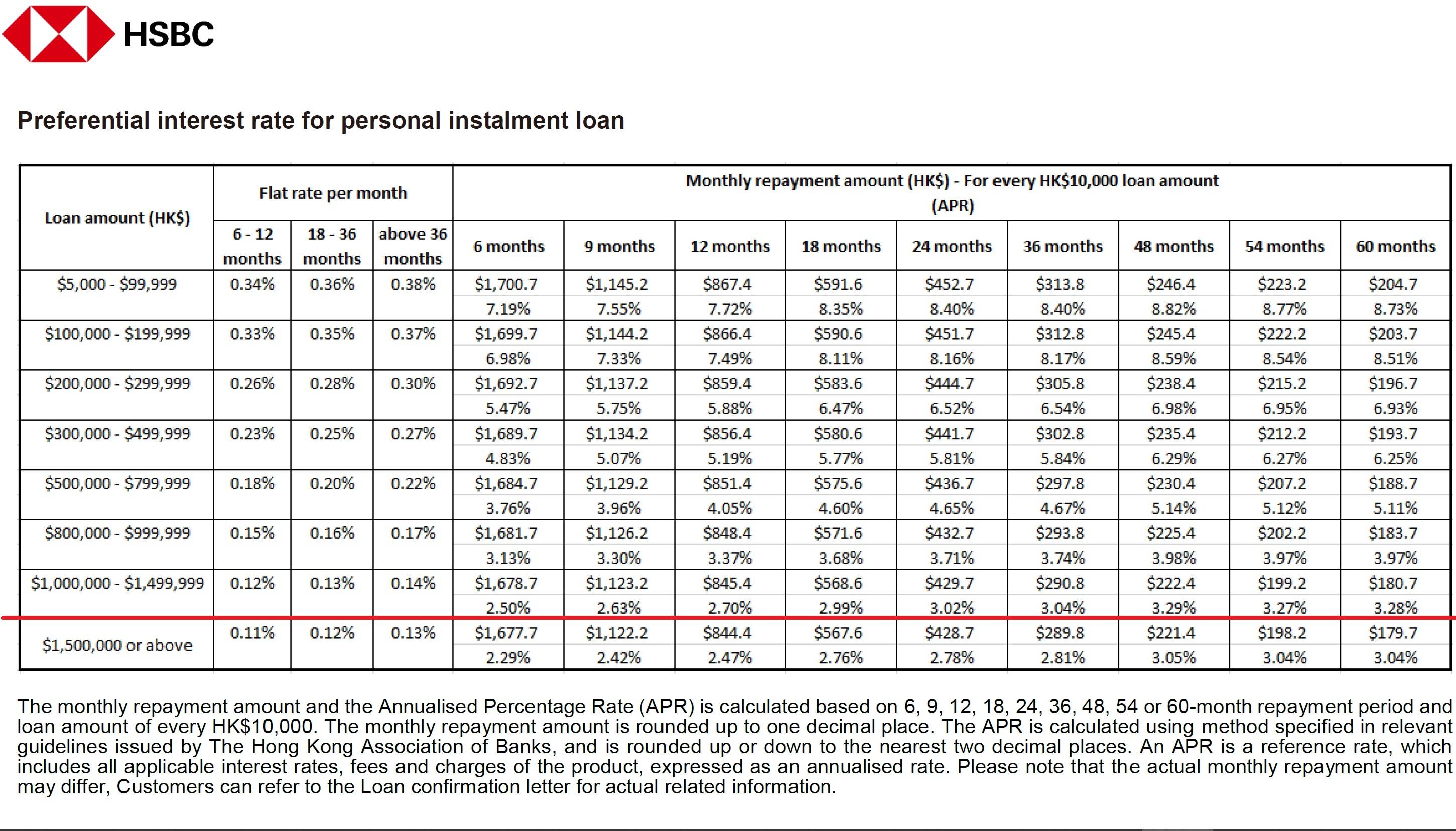

I screenshot picture beneath from HSBC HK. Scroll down a quarter of the way, and click on 'Rates' to download that PDF. I ask just about the last line on loans under red horizontal line.

Canadian ETFs with MERs < 0.15% like XUS (iShares Core S&P 500 Index ETF) can probably outstrip an APR of 6%.

Thus why would a wealthy bank loan at APRs < 6%?

Conversely, why don't they charge more than 6%? Why not charge the opportunity cost of loaning, that is, the APR gained from investing in a relatively safe ETF like XSP?

Furthermore, HSBC HK probably has PhDs in math like James Simons who can invest in alternative investments that can yield a higher rate of return for the same risk.