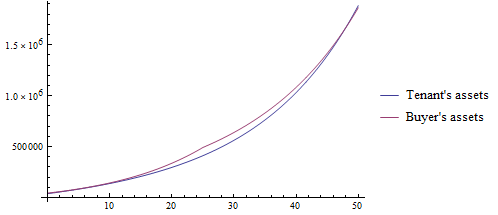

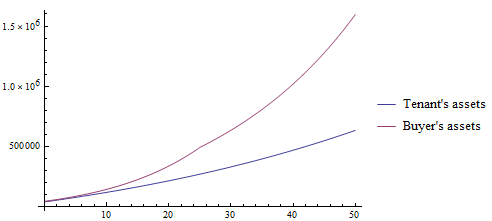

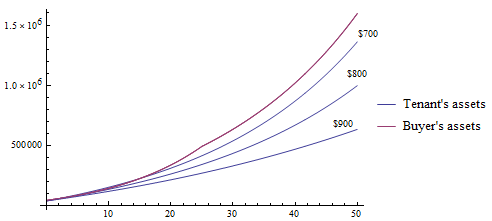

Similar question: In general, is it financially better to buy or to rent a house? which you can see the returns they are getting

Ok, so I'm wanting to know how I can calculate how profitable it would be to buy a house versus invest my money in a managed fund. I know this depends very much so on a case by case basis, but I'm interested in your both opinion on the matter/my circumstances and also ways in which I can calculate the value of my options (since you probably don't know the New Zealand market overly that well).

Some details about me:

- I'm 19 years old and a recent grad on a decent salary.

- I live in a little city in New Zealand.

- If I buy a property I would live in it for 1-2 years before travelling/working overseas and likely living in another city in New Zealand thereafter.

- I am able to have my parents manage the property as a rental which makes things significantly easier.

- I'm looking to buy a 3 bedroom house for approximately 300k

- There is a housing bubble in the capital city of New Zealand, I am a fair way away from that geographically, however I do not know how well it would affect things.

- New Zealand has no capital gains tax and they are unlikely to introduce it to affect somebody with only 1 home.

- If I did not buy a home I would likely invest in a managed fund such as Devon funds

- I presently do not have the full deposit, I have about a 13% deposit but it would not take me too long to acquire the amount I need.

- New Zealand has a superannuation scheme which I can get $5000 from as a free grant and I can also probably gain an additional $4000 from withdrawing my "employer contributions" from it (which I can do only if I'm buying my first home). So buying a house has about $9000 worth of added value for me.

I'm interested to hear your opinions regarding my situation and any advice you can give.

Cheers,

EDIT: Look at all of the answers, not just the accepted one as they are all excellent and provide very valid and sometimes case specific examples, however the accepted answer was simply the most satisfying answer for me personally.