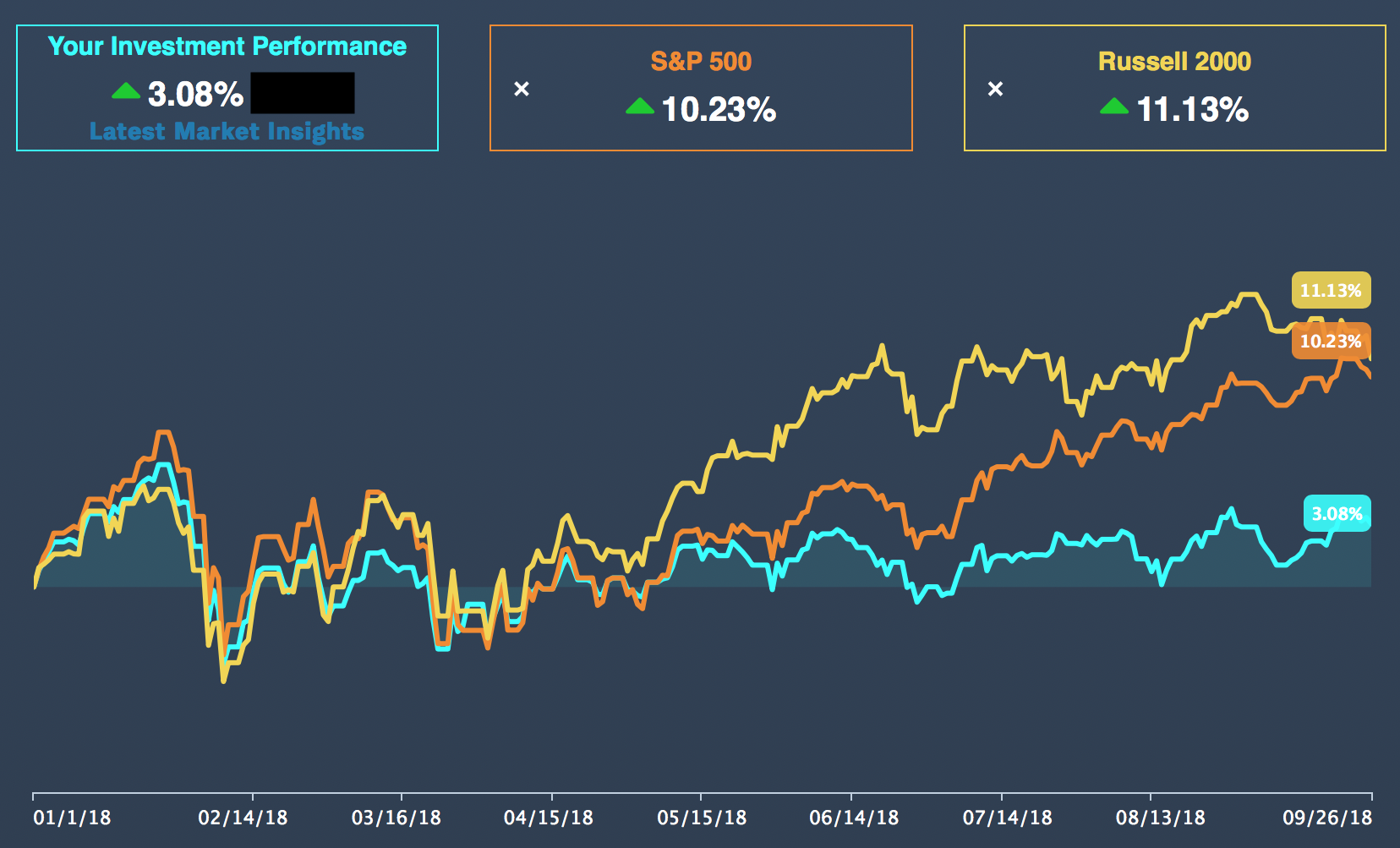

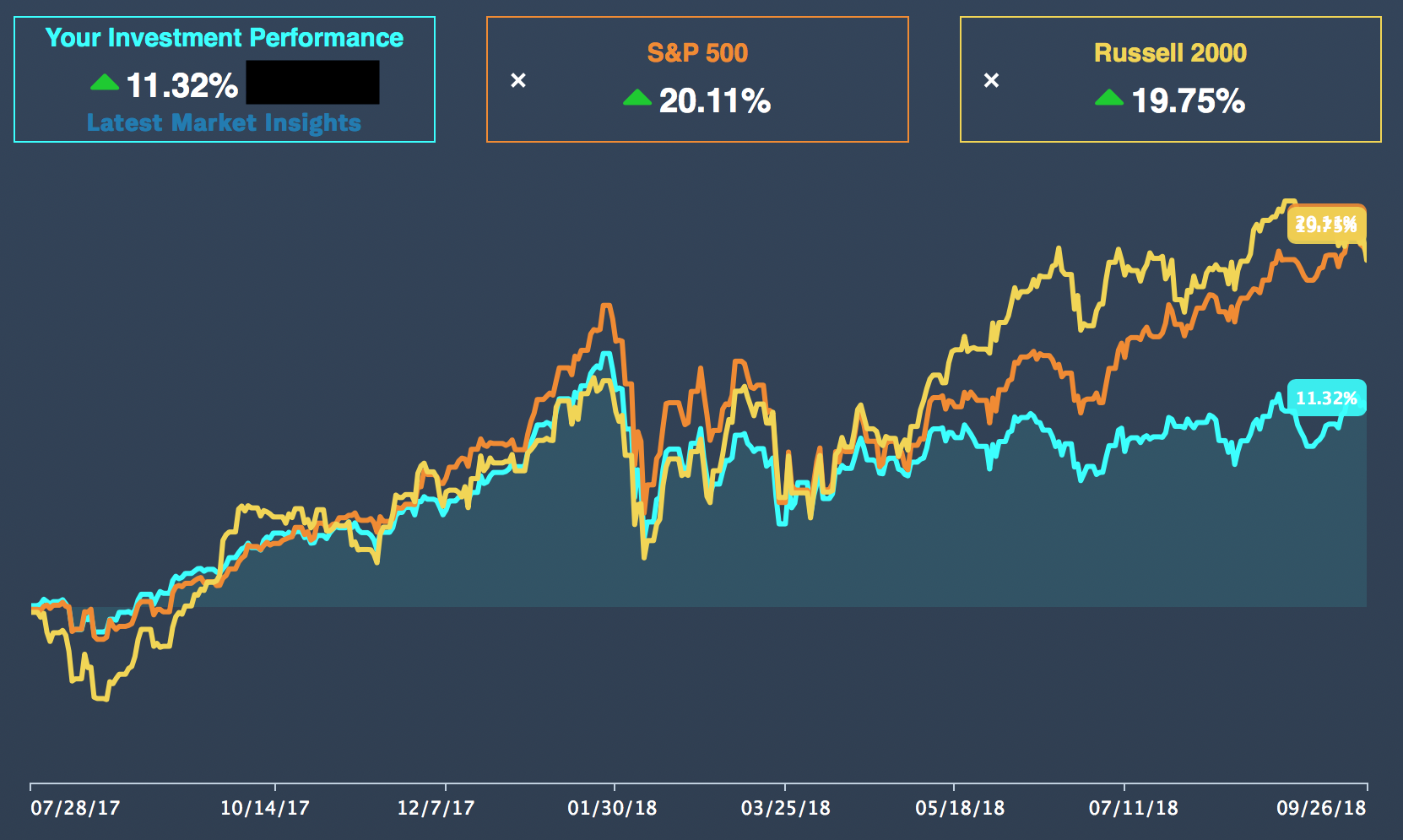

I like the idea of a Robovisor like the Schwab Intelligent Portfolio, Wealthfront, etc. But recently, my own experiences have been...a little worrisome. Despite the market being fairly bullish, and my portfolio set on the maximum risk setting, the performance of the portfolio has been starkly lacking compared to some other indexes, either for the year, or since the portfolios have been active.

That feels somewhat worrisome - is there something I'm missing about the performance and appeal of these?

Edit: Some folks have asked about details of the portfolio:

It's a Schwab Intelligent Advisor Portfolio, with the maximum risk tolerance settings on. The current allocation is:

Cash: 6.74% (Note this is something that's non-controllable in the allocation)

FNDX : SCHWAB FUNDAMENTAL US LARGE CO ETF 17%

FNDF : SCHWAB FUNDAMENTAL INL LARGE COM ETF 13%

SCHX : SCHWAB US LARGE CAP ETF 11%

FNDA : SCHWAB FUNDAMENTAL US SMALL COM ETF 11%

SCHF : SCHWAB INTERNATIONAL EQUITY ETF 9%

SCHA : SCHWAB US SMALL CAP ETF 7%

FNDE : SCHWAB FUNDA EMG MKTS LARGE COM ETF 6%

FNDC : SCHWAB FUNDAMENTAL INTL SMAL COM ETF 6%

SCHE : SCHWAB EMERGING MARKETS EQUITY ETF 4%

SCHC : SCHWAB INTERNATNAL SMALLCAP EQY ETF 4%

SCHH : CHARLES SCHWAB US REIT ETF 4%

VNQI : VANGUARD GLBAL EX US REAL ESTATE ETF 2%

IFGL : ISHARES INTERNATIONAL DEV RL EST ETF 0% - small, small amount