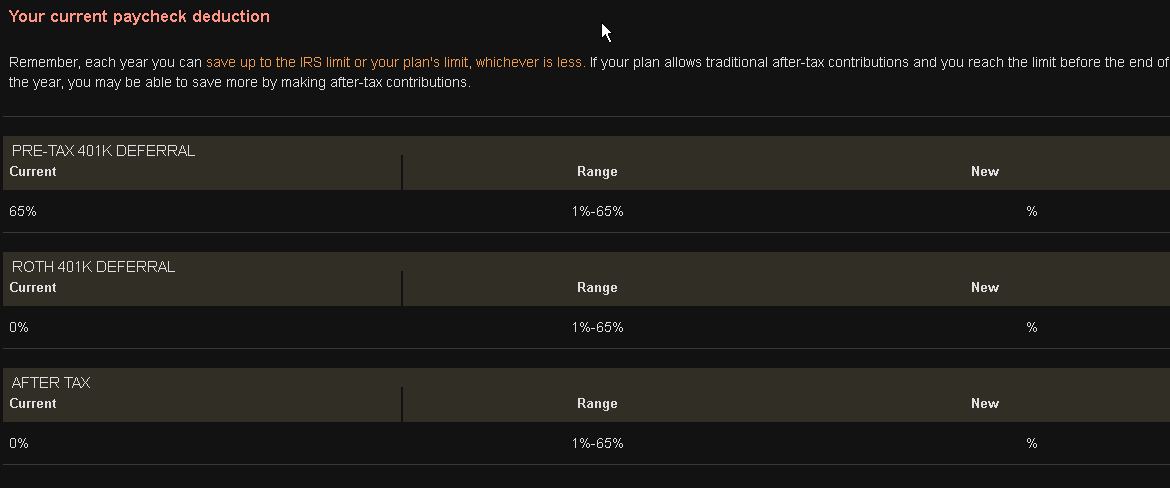

In some 401(k) plans, one has the choice to configure one's paycheck deductions to go to pretax 401(k), after-tax 401(k) and Roth 401(k):

Is there any upside to contributing to the after-tax 401(k) instead of the Roth 401(k) via paycheck deduction?

RelatedNotes: What are the pros and cons of converting an after-tax 401(k) to a Roth 401(k)?. In this new question, I'm focusing on the contribution aspect. For example, contributing to a Roth IRA isn't allowed for individuals with high income and one has to instead first contribute to the traditional IRA, then convert it into a Roth IRA.

- Related question: What are the pros and cons of converting an after-tax 401(k) to a Roth 401(k)?. In this new question, I'm focusing on the contribution aspect. For example, contributing to a Roth IRA isn't allowed for individuals with high income and one has to instead first contribute to the traditional IRA, then convert it into a Roth IRA.

- Vanguard (website where the screenshot above was taken) should have clearly written after-tax 401(k) instead of simply "after-tax".