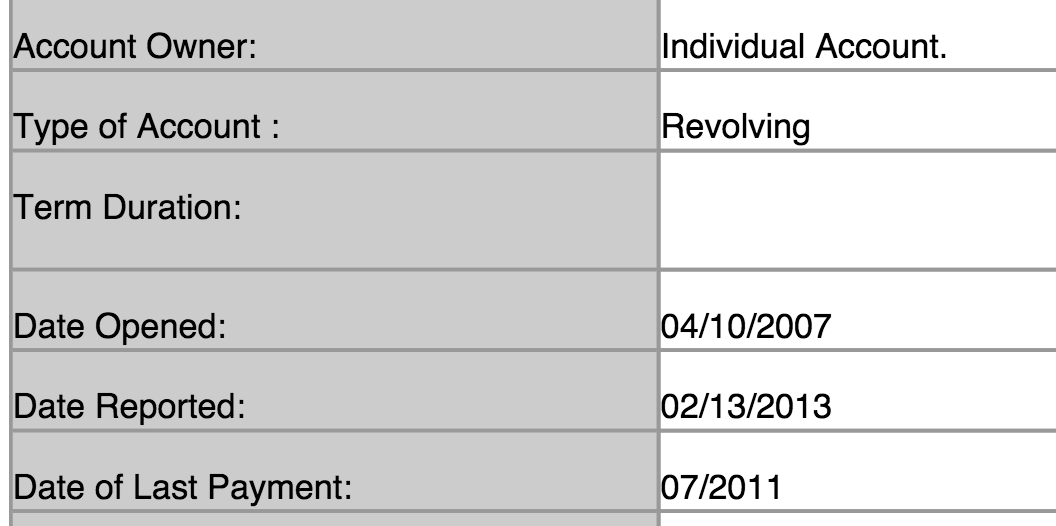

The answer to your question is that it is usually based on the last reporting date, i.e., the last activity date as reported by the creditor. The late payment itself may have been in 2011, but if the card or account was still active beyond that then the creditor would continue reporting until such time that the account was closed and went inactive. If you kept the card until 2013, that's the legitimate ending date for the creditor to be reporting.

The item is approaching 4 years old from the last reporting date, so its effect on your credit score is fairly minimal at this point anyway, and new, good credit will have a more powerful effect on your score.

Depending on the type of credit you're seeking, some creditors don't care much about negative credit that is more than 2 or three years old, especially if it is paid off, unless it is a substantial debt. In this case, you're talking about a single late payment. That's much different than a default on an account or a judgment from a court on a debt collection.

This is a minor blemish, and not much to be terribly concerned about at this late date. See it as a lesson learned about making timely payments and move on. What you're doing with credit now is far more important to potential creditors than the old stuff. If anything, the late payment may cause you to pay slightly higher interest or not qualify for some cards that demand high-quality credit scores, but that's not the end of the world.

I hope this helps.

Good luck!