First let's have a given to keep answers based purely on numbers, and away from opinions and advice on practicality:

- I am financially irresponsible

- I will get approved financing

- Most importantly, my financially responsible spouse will approve it!

How do you compute for losses on an upside down trade-in of a car, for purchase of a new car?

Current car to trade-in:

- Total of monthly payments made for 15-months: $8,505

- Down payment made: $4,750

- Trade-in value (estimated based on black book, 24,000 Km): $28,000

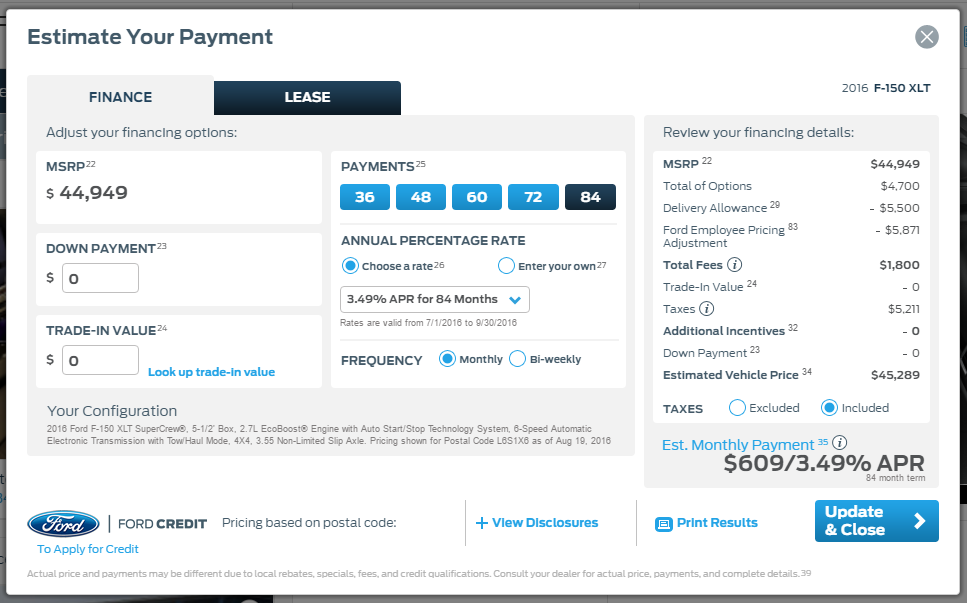

- Total obligation (all-in incl. taxes, 5% interest, 84-months): $48,500 [this was 'day 1' total obligation]

New car to purchase:

Basically, I'm thinking like this:

- I "sell" (trade-in) my car to the dealer for $28,000

- However, I still owe the financing company $35,245 (48,500 total obligation, less 8,505 total payments already made, less 4,750 downpayment)

- So $28,000 less $35,245 = ($7,245)

Meaning, trading in my current car, I immediately lose $7,245, not to mention I will start a new 84-month term. Is this correct?