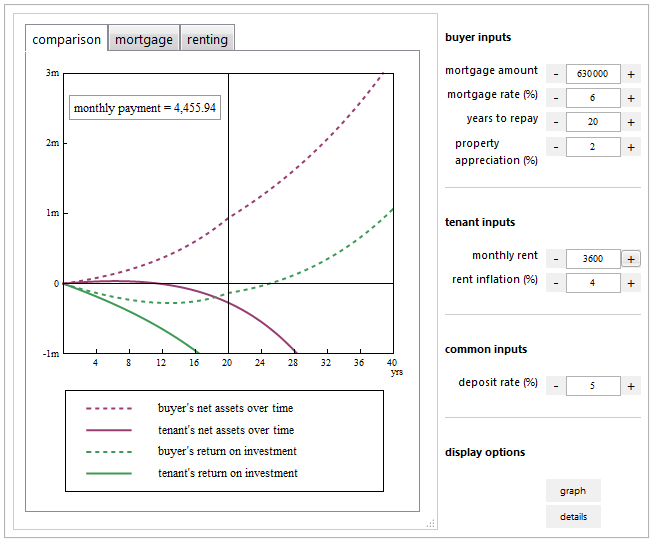

Option A: $3600 (RENT) for a 3/2.5 condo.

Option B: $629,000 (BUY) for a 3/1.75 house.

This is in the Los Angeles area.

Looking to live in this area for at least a year, maybe more. The house wouldn't be something we'd live in for 20 years or anything, but we could live there a few years then rent it out or sell.

According to my calculations:

1 year of rent = $43,200

1 year of owning = $25,000 in mortgage payments + $7800 taxes = $33,000 total.

Assuming we put 20% down on the purchase option.

So it seems like buying is the better option right? Saves $10,000 over the first year, and that doesn't even count any equity. It's just more risky - I guess the market could always take another dive and we'd lose money.

Is there anything else we should be thinking about? Any advice? Assume we like both properties equally.