I need to write a mock up application that returns a quote to potential borrowers. The specification says that "The monthly and total repayment should use monthly compounding interest".

Program input: Requested Amount, Rate, Loan length in months

Program output: monthly repayment, total repayment amount

This is the example they give:

Input:

Requested amount: £1000

Rate: 7.0%

Months: 36

Output:

Monthly repayment: £30.78

Total repayment: £1108.10

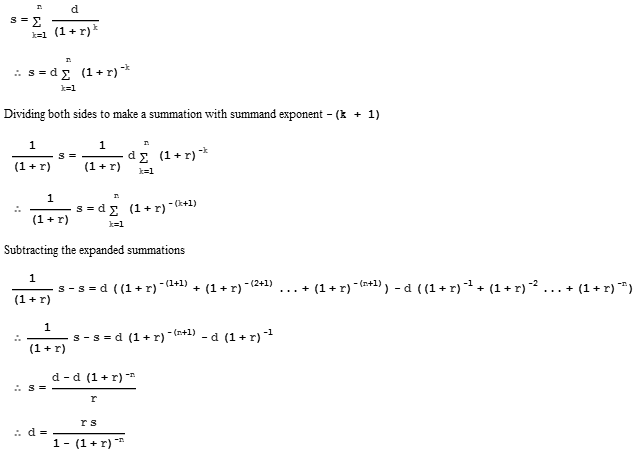

The problem is that I don't know how they arrived at this result. After consulting some websites, for example here. I found that the formula for calculating the compound interest rate is

A = P (1 + r/n) ^ nt

Where:

A = the future value of the investment/loan, including interest

P = the principal investment amount (the initial deposit or loan amount)

r = the annual interest rate (decimal)

n = the number of times that interest is compounded per year

t = the number of years the money is invested or borrowed for

Using this on our example we get A = 1000*(1+0.07/12)^(36) = 1232.92, which is not 1108.10 as they say in their example.

I am wondering if their example is wrong or am I missing something here

Thanks!