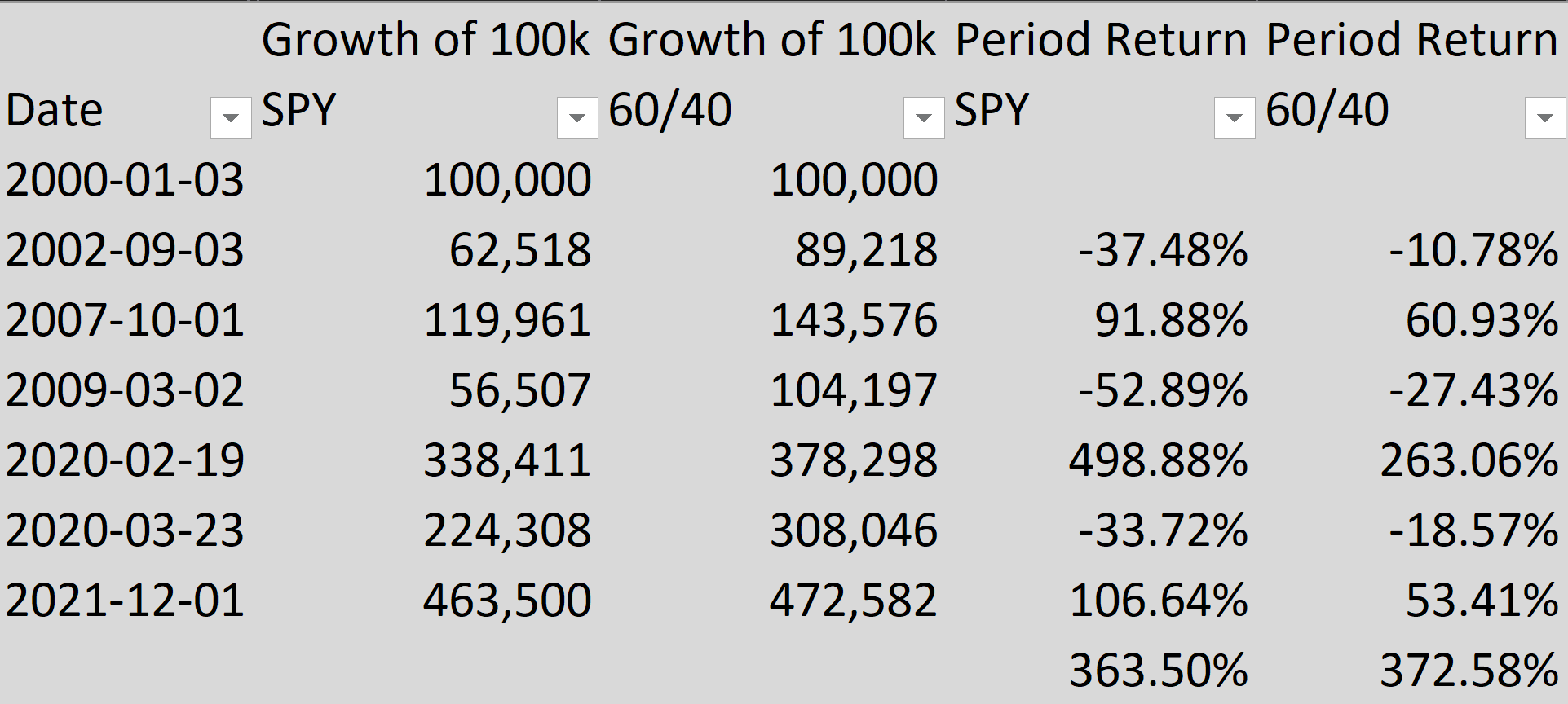

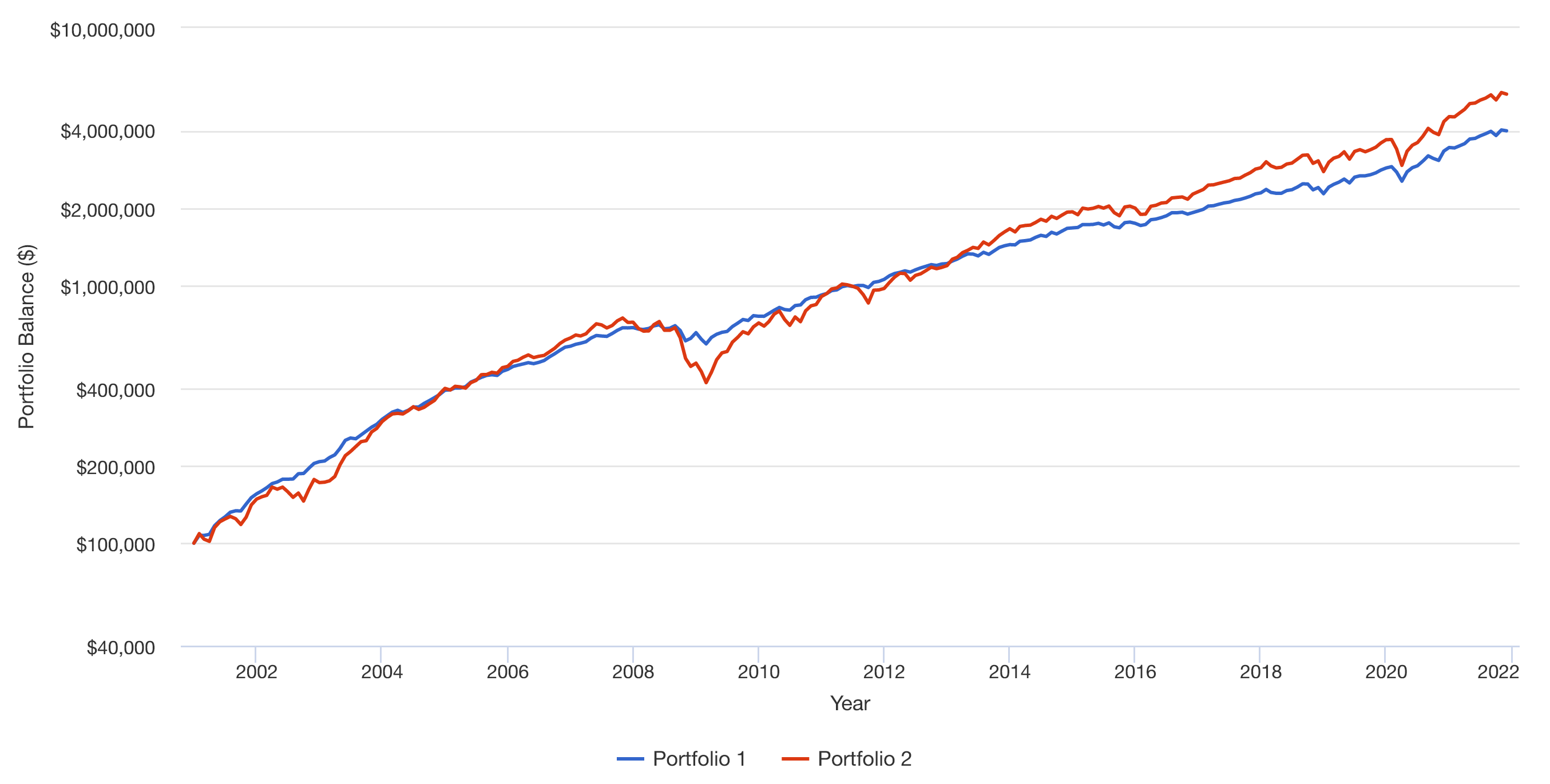

Final Edit: End Value of 60/40(10-Year Treasury) is worse than S&P 500.

Instead of blindly deriving the Bonds Fund price from Yield to Maturity, this time using the oldest available proxy to 10-Year Treasury Index (i.e. Lehman/Barclays/Bloomberg) which are the following Mutual Funds in 6:4 Ratio:

- Vanguard Intermediate-Term Treasury Fund Investor Shares (VFITX), duration 5.2 years, inception 10/28/1991

- Vanguard Long-Term Treasury Fund Investor Shares (VUSTX), duration 18.0 years, inception 05/19/1986

and:

- Vanguard Total Stock Market Index Fund Investor Shares (VTSMX), inception 04/27/1992

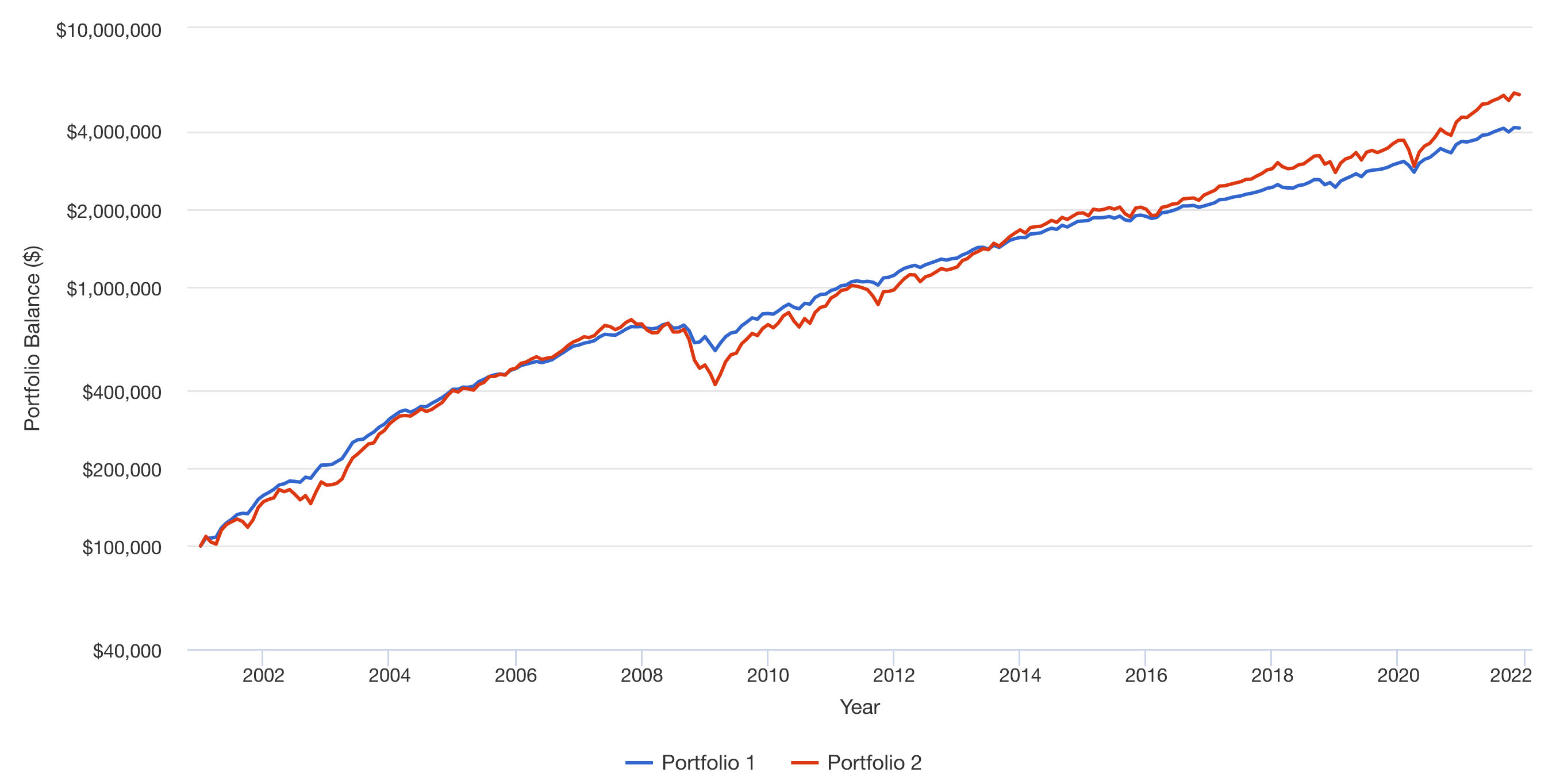

In the following charts:

- Portfolio 1 represents 60% S&P 500 (VTSMX), 24% VFITX + 16% VUSTX (10-year Treasury)

- Portfolio 2 100% S&P 500 (VTSMX)

Assume Montly Rebalancing because that is how balanced funds and the index works.

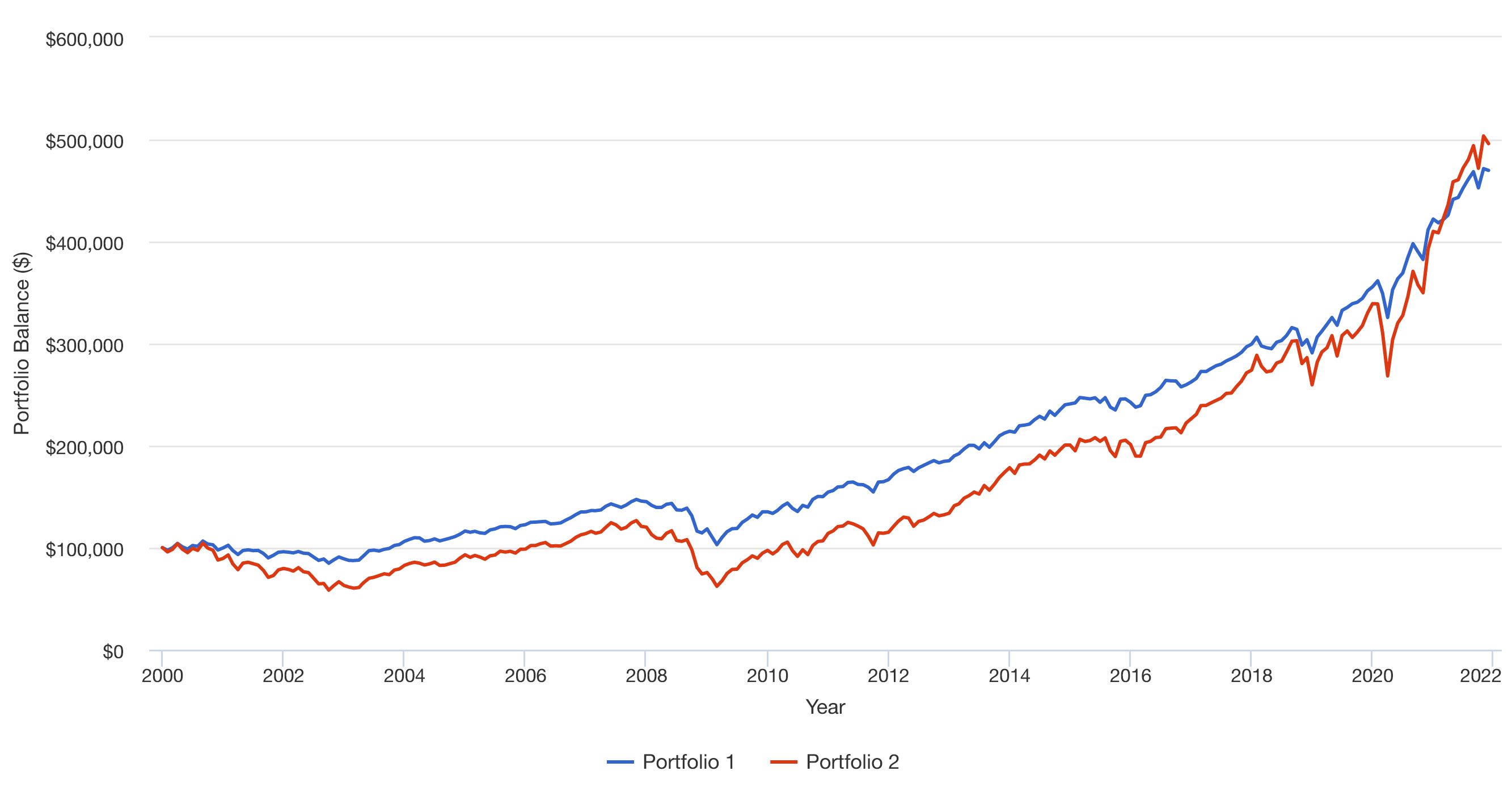

$100k Lump Sum with Monthly Rebalancing = False

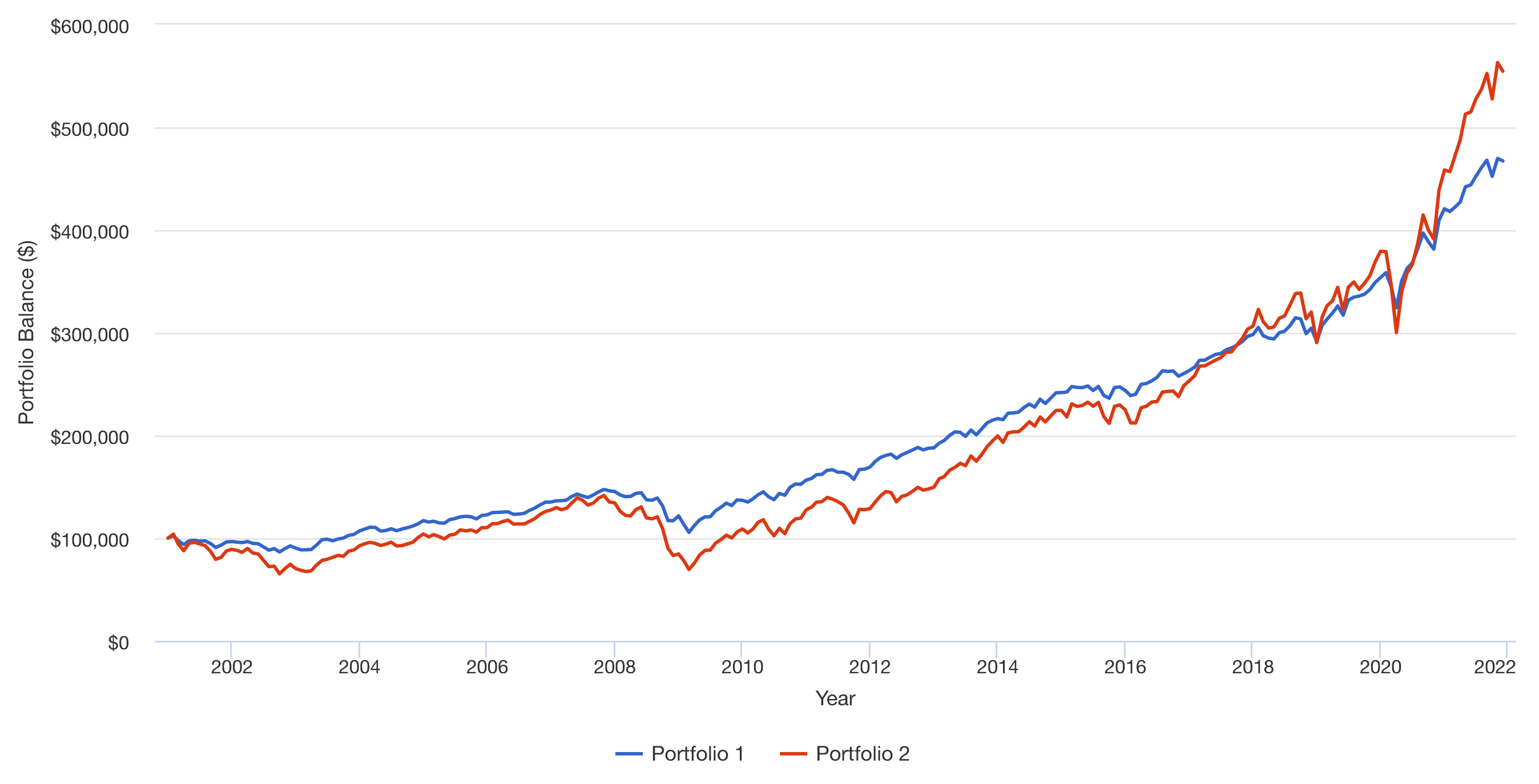

$100k Lump Sum and $5k Monthly Dollar Cost Averaging with Monthly Rebalancing = False

Edit: After discussing with the author on their assumptions.

$100k Lump Sum and $5k Monthly Dollar Cost Averaging with No Rebalancing = False

$100k Lump Sum and $5k Monthly Dollar Cost Averaging with Quarterly Rebalancing = False