Not safe at all. A 4% withdrawal rate would require the US stock market in the 21st century to produce returns similar to those of the 20th century, i.e. in the vicinity of 7% in real (inflation-adjusted) terms. Fair estimates for stock returns going forward are not this high. Rick Ferri proposed a real 5% over a 30-year horizon in 2015. I recall Bernstein in his book "Rational Expectations" (2014) proposing a real 3.6% over the very long term. These long-term estimates are based on the Gordon equation. According to this model, the long-term growth of a 100% SP500 stock investment in real terms would be the current dividend yield (~2%) plus the expected per share dividend growth rate (often given as 2%).

Bernstein's opinion on this subject is as follows: "Two percent is bullet-proof, 3% is probably safe, 4% is pushing it and, at 5%, you're eating Alpo in your old age [...] If you take out 5% and you live into your 90s, there's a 50% chance you will run out of money." (Source)

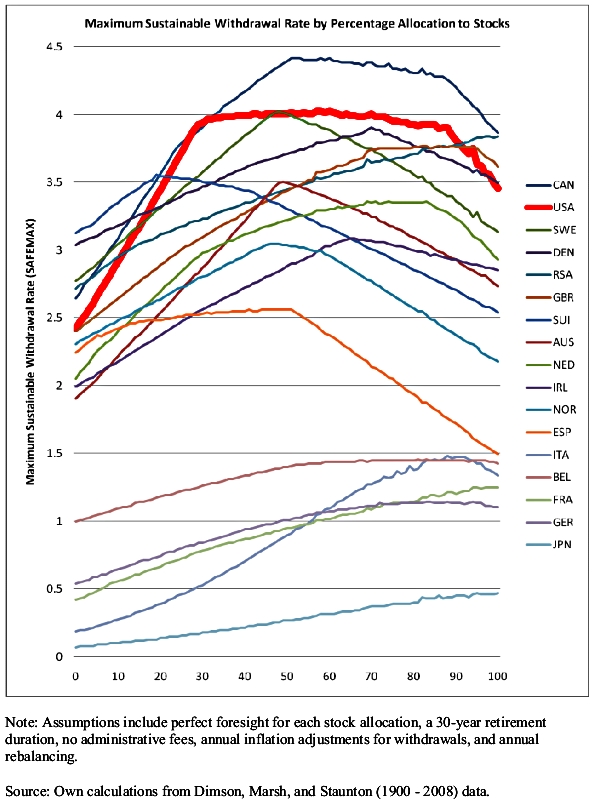

It is interesting to look at what happened to other countries in the past to get an idea of what could happen to the US in the future. The following graph shows the maximum sustainable withdrawal rate by percentage of allocation to stocks for various countries. The graph shows that despite the popularity of the "4% rule", very few countries could sustain a 4% withdrawal rate between 1900 and 2008 (before the crash) regardless of the stock/bond allocation. Even in those few countries, mainly the US and Canada, where it could work reliably, allocation mattered: At 100% stocks no country sustained a 4% withdrawal rate for every 30-year period in the 108 years of the data. Take a country that was not devastated by war in the 20th century like Switzerland or Australia. With a 100% stock allocation, 3% would have been too much for Switzerland but ok for Australia. With a 50/50 stock/bond allocation, 3.5% would have been too much for both countries.

It seems likely that the 21st-century US will do less well than the 20th-century US in terms of maximum sustainable withdrawal rates, given expected stock returns. Notice that except for Spain the countries that at some point failed to support a 2% withdrawal rate were all devasted by WW2. Spain had a civil war in 1936.

Image source: https://www.bogleheads.org/wiki/Trinity_study_update

Image source: https://www.bogleheads.org/wiki/Trinity_study_update