If the savings rate is the same as the loan rate, mathematically it doesn't make any difference whether you pay down the loan more and save less or vice versa.

However, if the loan rate is higher than the savings rate it's better to pay it down as fast as possible.

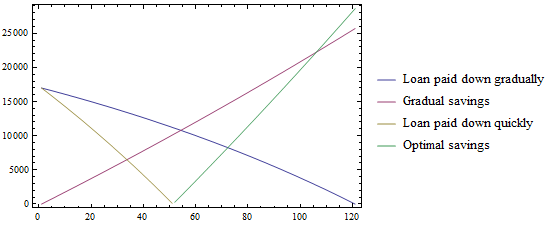

The chart below compares paying down the loan and saving equally (the gradual scenario), versus paying down the loan quickly at 2 x $193 and then saving 2 x $193. The savings rate, for illustration, is 2%.

Paying quickly pays down the loan downcompletely by month 51. On the other hand, in the gradual scheme thethe loan can't be paid down (with the savings) until month 54, which then leaves 3 months less for saving. In conclusion, it's better to pay down the higher rate loan first. Practically speaking, it may be useful to have some savings available.